「認識しているがだれも言及しない$700B」

Earlier this week, we observed that

as a direct result of a flood of Bill issuance in the past two months,

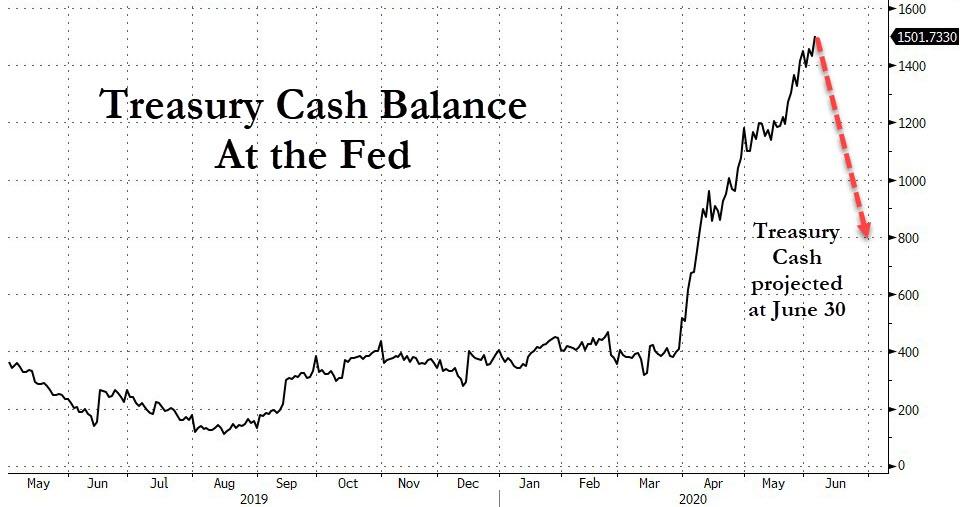

the Treasury's cash balance which it will use to fund various stimulus

programs and other fiscal initiatives, has exploded since the onset of

the coronavirus crisis, hitting a record $1.5 trillion last Friday.

This, we said, "is notable because in the Treasury's latest quarterly borrowing needs forecast which

projected a funding need of $3 trillion for the current quarter, the

Treasury also projected that the cash balance at the end of the quarter

would be $800 billion."

今週はじめのことだがZeroHedgeは気づいた、過去二ヶ月で多量のBillを発行したことの直接の影響だ、財務省のキャッシュバランスは本来各種経済刺激策に利用されるはずだ、これがコロナ危機以降爆発的に増えている、先週金曜にはなんと$1.5Tまで膨れ上がった。ZeroHdegeに言わせれば、この状況は特筆すべきもので、「財務省の最新四半期調達必要額は$3Tにもなる、また財務省は今四半期末のキャッシュバランスは$800Bになると予想している。」

This also means that if indeed the Treasury's forecast is accurate, then over the next two weeks, the Treasury's cash balance has to drop by a record $700 billion to hit the $800 billion target!

財務省の予想が正しいとするなら、今後2週間で、財務省のキャッシュバランスはなんと$700Bも減って目標値$800Bとなる!

Picking up on this quandary facing both the Treasury and the financial system, today Bloomberg writes that what the Treasury will do with its record $1.5 trillion pile of cash "has become the biggest wild card for funding markets as quarter-end approaches."

財務省にとっても金融システムにとっても難しい状況に直面している、今日のブルームバーグによると、$1.5Tものキャッシュを積み上げた財務省の行動が四半期末に向けての金融市場最大のワイルドカードとなる。

その理由をZeroHedgeが最初に議論したのは昨年のことだ、当時財務省のキャッシュバランスが9月に急増した、これが repo crisisのキッカケとなり、システムリザーブが直ちに引き出された、FED口座に預けている政府現金のスイングが「実行的に銀行リザーブを引き出すことになる」。

As a quick aside, the Treasury General Account which is published daily by the Treasury, operates like the government’s checking account at the Fed. When Treasury increases its cash balance, that’s on the liability side of the Fed’s balance sheet, so as that goes up, it drains reserves from the system In 2015, the Treasury instituted a policy of keeping at least five days’ worth of expenditures, or about $150 billion, in the account in case unexpected disruptions locked it out of debt markets. Before that, Treasury kept enough cash for just two days. But as the US budget deficit has begun to soar, the size of that buffer has grown.

余談だが、財務省一般口座は毎日公開されている、FEDの当座預金口座と同様だ。財務省がキャッシュバランスを増やすときには、FEDのバランスシートの負債側に対応する、というわけでこれが増えると、システムからリザーブを引き出すことになる。2015年に、財務省は少なくとも5日間の支出を手元に置くと主張した、もしくは約$150Bだ、予想外にこの口座の額が変動すると債務市場に影響する。この宣言以前には、財務省の手元資金はわずか2日間だけだった。しかし米国財政赤字が急増するに伴い、バッファー規模が膨れ上がった。

* * *

Echoing these our observations from Monday, today Bloomberg cautions that this dynamic "is taking on added meaning before quarter-end, with strains in the banking system already appearing to build in the lead-up to June 30. The big question now is whether the Treasury will stick to its end-of-June cash-balance target of $800 billion - about $700 billion below its current level."

月曜からのZeroHedgeno見立てに同調するように、今日、ブルームバーグが注意喚起を呼びかけた「この力学は四半期末前にさらなる意味を持つ、6月30日には前段階が表面化するだろう。現在の最大の疑念は、財務省が6月末のキャッシュバランス目標$800Bに固執して現在のキャッスバランスから$700Bも減らすかどうかだ。

To be sure, unlike last September, and the massive cash build observed since March when the Treasury pre-funded much of the upcoming stimulus payments, the concern is now in reverse as shrinking the balance would help ease any quarter-end stress by adding liquidity to the banking system, however "uncertainty is complicating decisions for participants in this key segment of financial markets - from managers of money-market funds, to hedge funds using it to generate liquidity through repurchase agreements."

念の為に言うと、昨年9月とは異なり、3月依頼巨額のキャッシュが積み上げられている、財務省が今後の刺激策のために事前に巨額の資金を供給した、現在の準備金の懸念は、バランス縮小は四半期末ストレスを緩和する、しかしながら「不確実性がこの金融市場で重要なセグメントでの判断を複雑にしているーーマネーマーケットファンドマネージャからヘッジファンドまで、だれもがレポ取引で流動性を生み出しているのだ。」

Indeed, as BMO's rates strategist Jon Hill says, "It’s like the $700 billion gorilla in the room" adding that "the Treasury has created a multi-hundred billion dollar level of uncertainty for the Fed’s balance sheet going into quarter-end. This is one of, if not the biggest, question over the next three weeks on how the front end plays out with regard to liquidity conditions."

たしかにそうだと、BMOの金利ストラテジストJon Hillはいう、「だれもが$700Bのことは承知している」更にこう加える「財務省は数百Bドルの不確実性を生み出した、四半期末に向けてのFEDバランスシートにおいてだ。これは大きな疑念の一つだ、今後三週間で流動性に関してどうなるか。」

言い換えるならば、誰もが疑問に思っていることで、ZeroHedgeが月曜に問いただした、「今後三週間の間に財務省は米国金融市場に$700Bの流動性を撒き散らすかどうか?ということだ」

While some have speculated that it will very difficult for the Treasury to allocate all those funds over the next two weeks, especially since there is virtually no demand for the remaining $140BN in unused PPP funds, on Thursday Steven Mnuchin sought to ease concerns, saying that more money is about to flow out of the government’s coffers. Of the roughly $3 trillion of pandemic relief, about $1.6 trillion has been used, and “we’re busy working on disbursing the rest of the money,” he told reporters in a video conference.

今後2週間農地に財務省がこれらの全資金を利用するかどうかの判断はとても難しいと言う人もいる、特にPPPファンドはまだ利用していない資金が$140Bもあり需要は殆どないとも言える、しかしながら、水曜にSteven Munchinは懸念を緩めようとした、彼が政府金庫からさらに資金を放出すると言ったのだ。パンデミック対策費$3Tのうち、約$1.6Tはすでに利用された、そして「残りの資金の配分にとても忙しい」とビデオ会議でリポーターに話した。

"There’s a lot of money that hasn’t been allocated” yet, and over the next month $1 trillion will be pumped into the economy, he said. It was, however, not clear just how this money would be "pumped into the economy."

「まだ支払われていない資金はたくさんある」それでも今後一月で経済に$1Tを注入する、と彼は言った。しかしながら、この資金がどのようにして「実際に経済システムに注入されるか」は明確ではない。

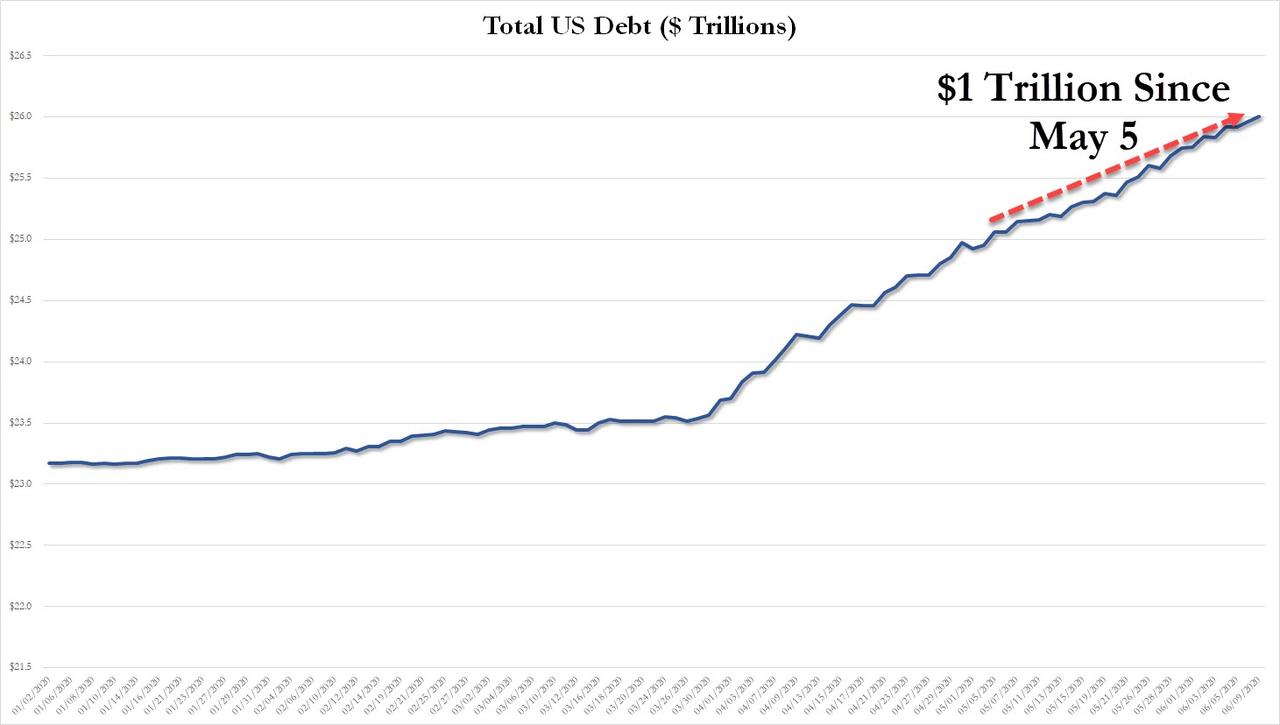

The problem, as Bloomberg notes, is that while investors have been able to absorb the record barrage of new debt, which has seen US Federal Debt increase by $1 trillion in the past month, rising above $26 trillion for the first time ever this week...

問題は、ブルームバーグも指摘するように、投資家がこの記録的な量の新規債務を吸収してきたが、米国連邦債務はこの一月で$1Tも増えたわけで、今週には過去最高を更新して総額$26Tにもなるということだ・・・

... with relative ease, signs of funding dysfunction are starting to emerge.

・・・これまでは比較的容易に吸収してきた、資金提供がうまくゆかない兆候が現れ始めた。

その一例が、3ヶ月もの政府債務証券金利と一夜ものswaps金利のスプレッドだ、この値は政府債務調達市場の健全性指標となる、これが4月依頼とても悪化している。大統領は政府のmねーマーケットファンドから資金を提供するがーーここ数ヶ月現金に陰りが見えるーーT-billsやレポ市場への投資が陰りを見せている、このために金利が高くならざるを得ない。多くの人が懸念を持つ最大の理由はこれだ、レポ市場の「グル」と言われるZoltan Pzsarもその一人であり、FEDは今後数ヶ月YCCを諦めざるを得ないと推測している、短期金利のスパイクを抑えざるを得ないからだ。

DB strategist Steven Zeng, disagrees with Mnuchin and considers it unlikely that government outlays will prove large enough by month-end to drive the cash balance below about $1 trillion, meaning that the Treasury cash balance on June 30 will be far higher than what the government projected at the start of May, potentially reducing the need for more debt issuance.

Keeping the extra cash on hand will also allow Treasury to capitalize on having tapped the money already at very low rates. However, sooner or later that money will have to hit the broader economy: "It’s not that the money won’t be spent, it’s just a matter of the timing."

Of course, it the Terasury is right, and "if the $700bn actually leave the account at Fed and flow into the real economy before quarter-end, then it is likely a massive boost for risk assets" Nordea's Andreas Steno-Larsen wrote last weekend.

DB strategist Steven Zeng, disagrees with Mnuchin and considers it unlikely that government outlays will prove large enough by month-end to drive the cash balance below about $1 trillion, meaning that the Treasury cash balance on June 30 will be far higher than what the government projected at the start of May, potentially reducing the need for more debt issuance.

DBストラテジストのSteven ZengはMnuchinの方針に否定的だ、米国政府は月末までにキャッシュバランスを$1T以下にするほどに巨額の資金を利用できないだろうと見ている、ということは5月初めの政府見立てとは異なり6月30日時点の財務省キャッシュバランスはもっと大きいと見ている、ということでさらなる債券発行の必要性は少なくなる。

Keeping the extra cash on hand will also allow Treasury to capitalize on having tapped the money already at very low rates. However, sooner or later that money will have to hit the broader economy: "It’s not that the money won’t be spent, it’s just a matter of the timing."

財務省はすでに多額の現金を手にしていることですでに低金利の市場からさらなる資金調達が可能だ。しかしながら、遅かれ早かれそれらの現金も幅広い経済に投入されるざるを得ないだろう:「その資金は使われないわけではない、単に時間の問題だ。」

Of course, it the Terasury is right, and "if the $700bn actually leave the account at Fed and flow into the real economy before quarter-end, then it is likely a massive boost for risk assets" Nordea's Andreas Steno-Larsen wrote last weekend.

当然のことながら、財務省の主張は正しい、そして「もし$700Bが実際にこの四半期末までにFED口座から出てゆくとすると、リスク資産に対して強力なブースト作用を及ぼすだろう」とNordea社のAndreas Steno-Larsenは先週述べた。

In any case, as we concluded on Monday, it is still not immediately clear just how the Treasury could deal with this "$700 billion gorilla in the room" and ram this cash into the real economy: as a reminder, roughly $140BN of the latest iteration of the Paycheck Protection Program remains unused as business demand for what is effectively free money in the form of grants, appears to have peaked. Will the Treasury then proceed with literally paradopping tens of billions in cash on Americans? To be sure, that would be one way to make the protests across America a far more festive event.

In any case, as we concluded on Monday, it is still not immediately clear just how the Treasury could deal with this "$700 billion gorilla in the room" and ram this cash into the real economy: as a reminder, roughly $140BN of the latest iteration of the Paycheck Protection Program remains unused as business demand for what is effectively free money in the form of grants, appears to have peaked. Will the Treasury then proceed with literally paradopping tens of billions in cash on Americans? To be sure, that would be one way to make the protests across America a far more festive event.

どちらにしろ、ZeroHedgeが月曜に結論づけたように、「誰もが認識しているこの$700B」を財務省がどう処理するかはすぐに明らかになるわけではない:念の為に言うと、Paycheck Protection Programはまだ$140Bをまだ消化していない、政府援助で自由に使える資金だ、すでにピークを超えている。財務省は文字通り数十Bの現金を米国中にばらまくだろうか?念の為に言うと、これは全米のさらなるお祭り騒ぎに対する抗議とも言えるかもしれない。