次の十年ゼロリターンと、どうしてCredit Suisseは見ているか

人によって多様な見方があるからこそ相場が形成されます。皆さんはどう見ます?

Why Credit Suisse Sees 0% Returns Over The Next Decade

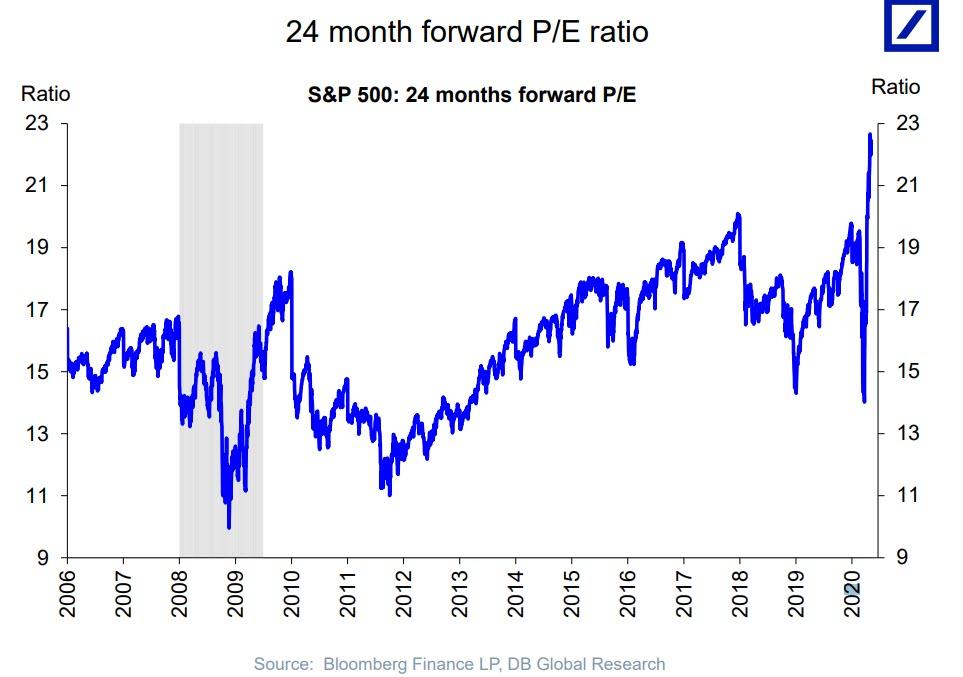

下に示すチャートはSP500の2年先(一年先ではない)Forward P/Eを示す、すなわち、2021年12月31日のEPS予想に基づくものだ、これがいまでは奇妙なことにこのチャートが自然な形にならない、これは特筆すべきことだ。

And while one can argue that nobody cares about fundamentals in a world in which the economy, profits and markets all exist in a state of what BofA called a "Schrödinger Equilibrium" created by the Fed, Credit Suisse equity strategist Jonathan Golub just has trouble believing that we now live in a world in which PE multiple have reached a persistently higher plateau.

だれもが指摘することだが、ファンダメンタルズに言及する人は居ない、経済、収益、市場環境においてだ、BoAに言わせれば今の市場は、FEDが生み出した「シュレディンガーの猫」状態だ、Credit Suisseの株式ストラテジスト Jonathan Golubはこれは問題だと確信している、いまや誰もがPERが常に高台状態にあるという世界にいると思いこんでいる。

As he writes in his daily note to clients today, "we’ve repeatedly made the case that more cash flow-rich companies, in a less volatile environment, would lead to a new regime of persistently higher multiples and the secular outperformance of growth and long-duration (less volatile) equities."

彼は今日、顧客向け日報でこう書いた、「私どもは繰り返しこう主張してきた、変動がそれほどでもない環境においては、よりキャッシュフローの良好な企業が持続的に高PER状態を生み出し、長期的には株式市場で良いパフォーマンスを示すと。」

Golub then counters that while "bearish investors would (correctly) point out that future returns are highly influenced by starting valuations, with higher P/Es leading to weaker performance, as multiples de-rate toward long-term averages", he would, in turn, respond that "valuations have little influence over the near-term" (the chart above makes that quite clear).

ところがGolubはそれに反してこう主張する、「弱気投資家の主張では、将来のリターンは投資開始時のバリュエーションに大きく依存するかもしれない、高PER銘柄に投資するとリターンは弱い、長期的にはPERは平均値に向かうからだ」というなかで、彼はあえてこう言う「短期的リターンにバリュエーションはほとんど影響しない」(上のチャートを見れば明らかだ)。

それでも、Golubはこう示唆する、これまで懐疑的であった投資家もだんだん高PERを心地よく受け入れ始めている、そして今や個人投資家が価格形成に重要となる中でこれは驚くことではない、しかしながら彼はいまだ「現在の相場背景を確信できないでいる」。

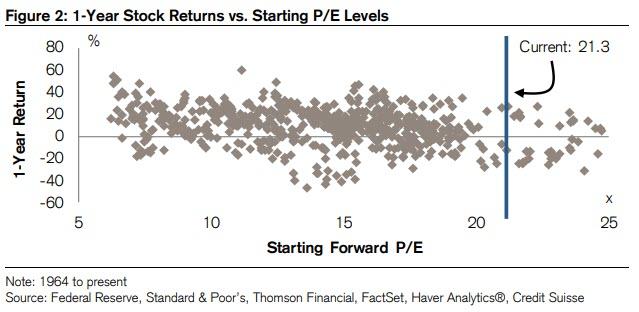

And just to underscore his point, Golub shows that whereas valuations indeed have little impact on 1-year stock returns...

彼の主張を強調するために、Golubはこのチャートを示す、1年後の株式リターンに関してはバリュエーションはほとんど影響しない・・・・・

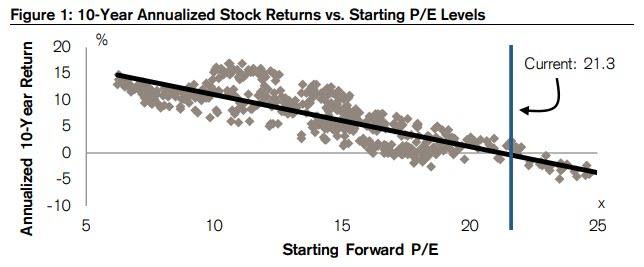

... they certainly impact the market's return over the coming decade. And as the second chart shows, when starting at the currently lofty valuation, returns over the next ten years tend to be more or less the same: 0%.

・・・・ところが10年後のリターンを見るとたしかに大きな影響がある。それが下のチャートだ、現在のようにそびえ立つほどのバリュエーションで投資を始めると、その後10年のリターンは変わらずだ:0%。