「根拠なきおまじない」ーー心配するな、FEDは「ベルトもサスペンダーも」してるから

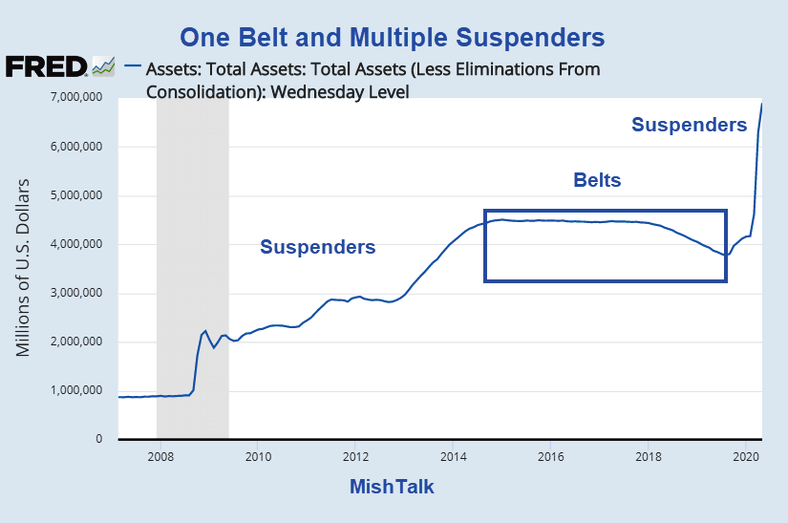

The Fed's balance sheet is approaching $7 trillion dollars. This is what Bernanke meant by suspenders.

FEDのバランスシートは$7Tに迫っている。これこそBernankeがサスペンダーにたとえたものだ。

On February 27, 2013, Ben Bernanke spoke to US Congress about how the Fed would unwind its balance sheet.

2013年2月27日に、Ben Bernankeは米国議会証言でFEDが如何にバランスシート巻き戻しをするかの証言を行った。

Bernankeが言うには、我々はバランスシート巻き戻しのための「ベルトもサスペンダー」も有るという。

Bernanke’s vague answer to Sen. Richard Shelby, R-AL, when asked how the Fed will deleverage the balance sheet, was this: “In terms of exiting from our balance sheet… a couple of years ago we put out a plan; we have a set of tools. I think we have belts, suspenders – two pairs of suspenders. I think we have the technical means to unwind at the appropriate time; of course picking the exact moment to do, of course, is always difficult.”

Bernankeは議会でRichard Shelbyの質問に曖昧に答えた、彼の質問はこうだ、FEDはどうやってバランスシートを縮小するというのだ、その答えは:「バランスシート膨張に関して、我々は2年ほど前に出口戦略を考えた;一連のツールがある。我々はベルトもサスペンダーも持っているーーサスペンダーは二組もある。適当なタイミングで巻き戻す手法がある;当然それは最適なタイミングで行わねばならない、そのタイミングを見計らうのが難しい。」

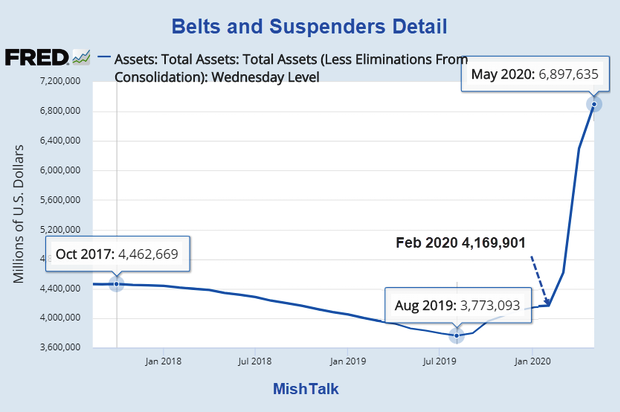

Belts and Suspenders Detail

ベルトとサスペンダーの詳細

Belts and Suspenders Synopsis

ベルトとサスペンダーの詳細

-

Belt tightening took the Fed's balance sheet from $4.46 trillion to $3.77 trillion.

ベルトでFEDバランスシートを引き締めた、その規模は$4.46Tから$3.77Tへの引き締め。

-

Suspenders took the Fed's balance sheet from $3.77 trillion to $6.90 Trillion in just 9 months.

サスペンダーでFEDバランスシートを$3.77Tから$6.90Tへとわずか9ヶ月で膨らませた。

Tapering, That's All You Get

テーパリングはこれだけだった

Please recall the September 18, 2019 QE Debate: What Did Powell Mean by "Need to Resume Balance Sheet Growth"?

2019年9月18日のQEに関する議論を思い起こしてほしい:「バランスシート膨張を再開する」としてPowellの意図はなんだったのか?

Powell's Prophecy

Powellの予言

"And we are going to be assessing the question when it will be appropriate to resume the organic growth of our balance sheet."

「そして我々はその時を見計らっている、バランスシートの自然 organic な膨張をいつ再開するのが適当か。」

More prophetic words have seldom been heard.

これ以上に予兆的な言葉を聞くことはまず無いだろう。

Some objected to my post because of the word "organic". I commented.

この言葉「organic」に異論の有るところだ。私はこうコメントした。

The Fed may do a brief period of "organic" expansion (which by the way can mean anything the Fed wants), but I propose more QE is coming whether the Fed "intends" to do so or not.FEDは短期的に「organic」な拡大を試みたかもしれない(ほかでもないFED自身が望んだのだ)、しかし私はFEDの「意図」に関わらずさらなるQEがやってくると思った。

Fed's 2019 Interest Rate Expectations vs Market's Expectations

Here's a look at the Fed's 2019 Interest Rate Expectations vs Market's Expectations

2019年のFEDの予想金利 vs 市場期待値を見てみよう。

これがそのドットプロットだ。

I propose the Fed is wrong, again, as usual.

いつものことだが、またもやFEDが間違っていると私は申し上げた。

For discussion of today's FOMC decision, please see Fed Cuts Rates 1/4 Percent, Three Dissents: Dot Plot Suggests No More 2019 Cuts

今日のFOMC決断に至る議論に関して言えば、 FEDは1/4パーセント金利を引き下げる、これが3回だ;ドットプロットには2019年の切り下げを示唆していない。

Dot Plot September 26, 2018

2018年9月26日のドットプロット

That's quite a hoot isn't it?

ちょっと笑えるじゃないか、ねえ?

Even without Covid-19, the Fed was not remotely close to its expectations.

武漢コロナが無くとも、FEDはまったく予想が外れている。

My Dot Plot comment at the time: "I side with those who expect more rate cuts."

当時の私のドットプロットに対するコメントはこういうものだった:「私はさらなる金利引下げが有ると見ている。」

Clueless Wizards

根拠なきおまじない

この根拠なきおまじないを信じ切る人もいる。一方で、FEDは市場期待に応じるしか無い、と考える人も多数だ。

However, this creates what would appear at first glance to be a major paradox: If the Fed is simply following market expectations, can the Fed be to blame for the consequences?

しかしながら、この状況には大きな矛盾を含んでいる:もしFEDが単に市場期待に応じるだけなら、その結末についてFEDを責めることができようか?

更に指摘するなら、FEDが単に市場期待に応じるだけなら、どうして市場が責められることがあろうか?これはとても興味深い理論的疑念だ。

Fed Uncertainty Principle

FEDの不確実性対応原則

私は上に述べたようなパラドックスについて議論する、もしFEDが市場期待に沿うだけなら、どうして金利はマイナスにならないのだろう?

Corollary number one stands for the for plot example above.

これらから導かれる当然の帰結はこうだ。

Corollary Number One帰結1

The Fed has no idea where interest rates should be. Only a free market does. The Fed will be disingenuous about what it knows (nothing of use) and doesn’t know (much more than it wants to admit), particularly in times of economic stress.金利がどう有るべきかについてFEDは自らのアイデアを持っていない。ソレを知るのは自由市場のみ。FEDは自らよく熟知しているかのように振る舞うだろう(やくたたずだが)そして実際には全く解っていない、特に経済的ストレスが高いときにはどうして良いかわからないのだ。

In case you missed the post, please give it a look. There's lots more in play regarding what the Fed knows and doesn't.

もし私のかつての記事を見落としているなら、もう一度見てほしい。FEDが知っていること知らないことについてもっと議論している。

Message From Gold

ゴールドが教えてくれること

もう一つの一対のサスペンダーが待ち構えている。

Gold has that message. Do you?

ゴールドが主張していることだ。あなたはどう思います?