Here is an example of a curve that everyone wants to flatten.

これは一例だが、だれもが曲線の平坦化を望んでいる。

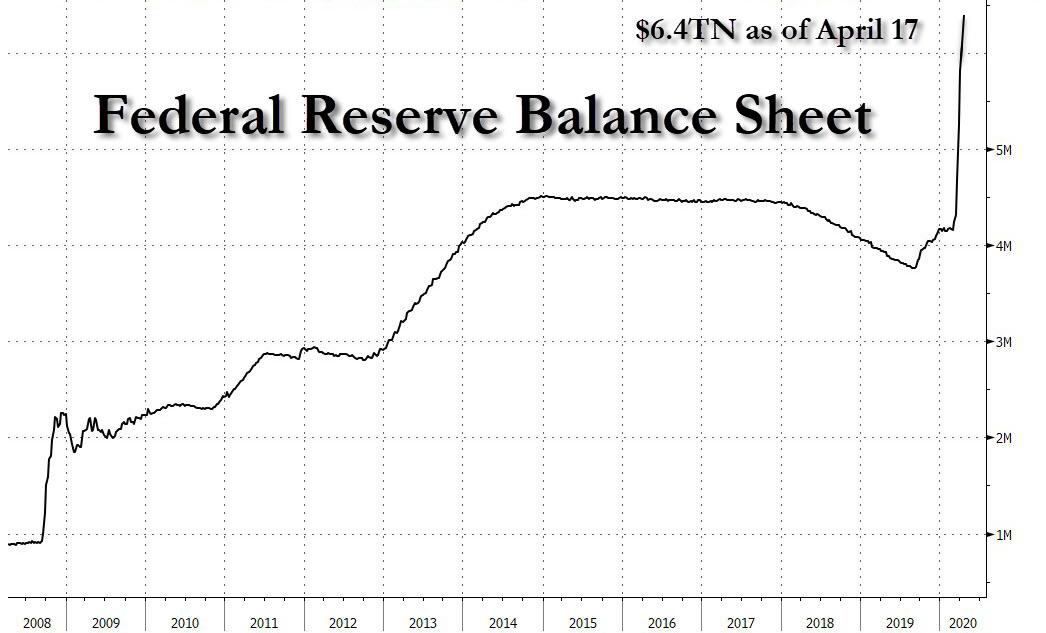

And here is an example of a curve that while some - namely the bears

- also wants to see collapse, it will never do so as that would mean

the end of western civilization - which is now entirely contingent on

the level of the S&P500 - as we know it. We are talking of course,

about the Fed balance sheet which is now well above $6 trillion to make

sure stocks and bonds don't crash.

With that in mind here is all you need to know about this particular "curve":

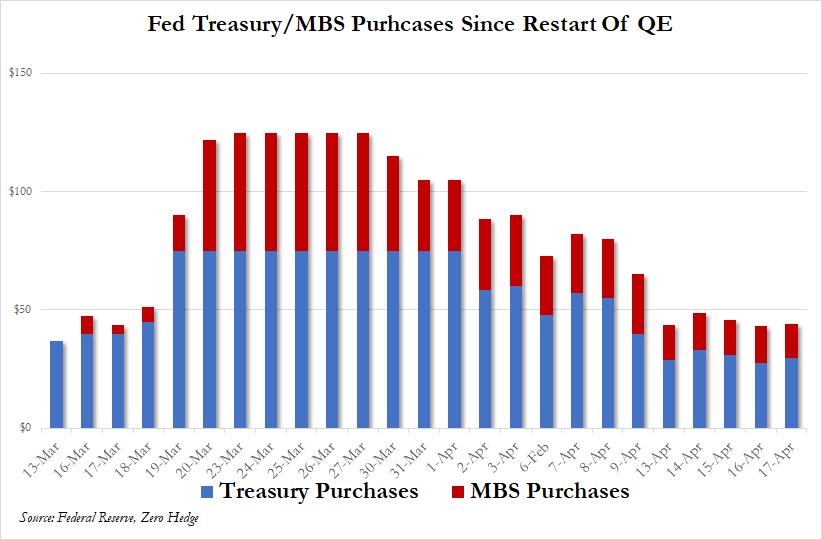

Total Fed assets grew by $293Bn to $6.08 trillion as of close, April

8, with the increase primarily driven by $294bn of Treasury securities

added to the SOMA portfolio. Through its credit facilities, the Fed also

extended $680bn in temporary liquidity to various counterparties, a

decline of $61bn from last week.

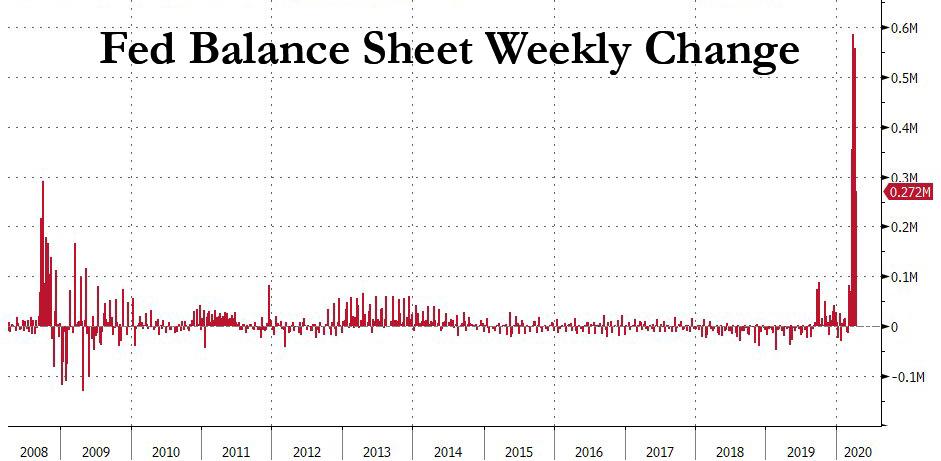

In the past month, the Fed balance sheet

has increased by $2 trillion, more than all of QE3, when the balance

sheet increased by $1.7 trillion over the span of a year. The balance

sheet increase has also been faster on a weekly basis than anything

observed during the financial crisis, increasing as follows:

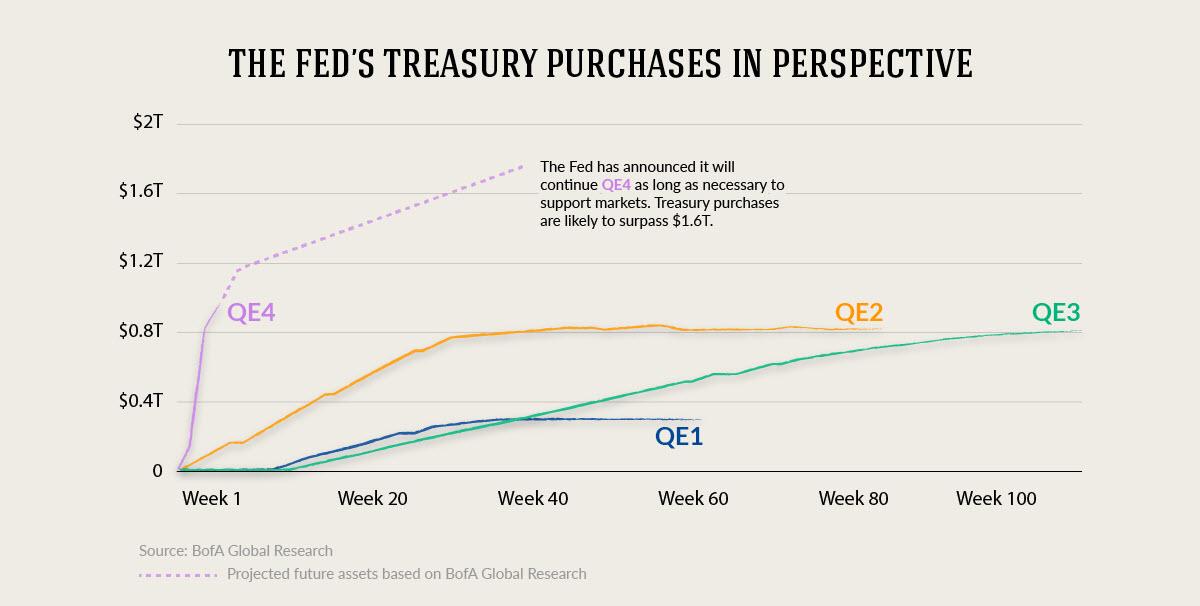

Since the Fed needs to monetize all debt issuance this year, and probably every other year now that the Treasury and Fed have merged and helicopter money has arrived, the pace of the current QE is like nothing ever observed before:

.. we can calculate that by next Friday, April 17, the Fed's assets will rise to at least $6.4 trillion,

almost double where the balance sheet was in early September 2019, just

before hedge funds needed to be bailed out and the Fed pretended like

it was saving the repo market.

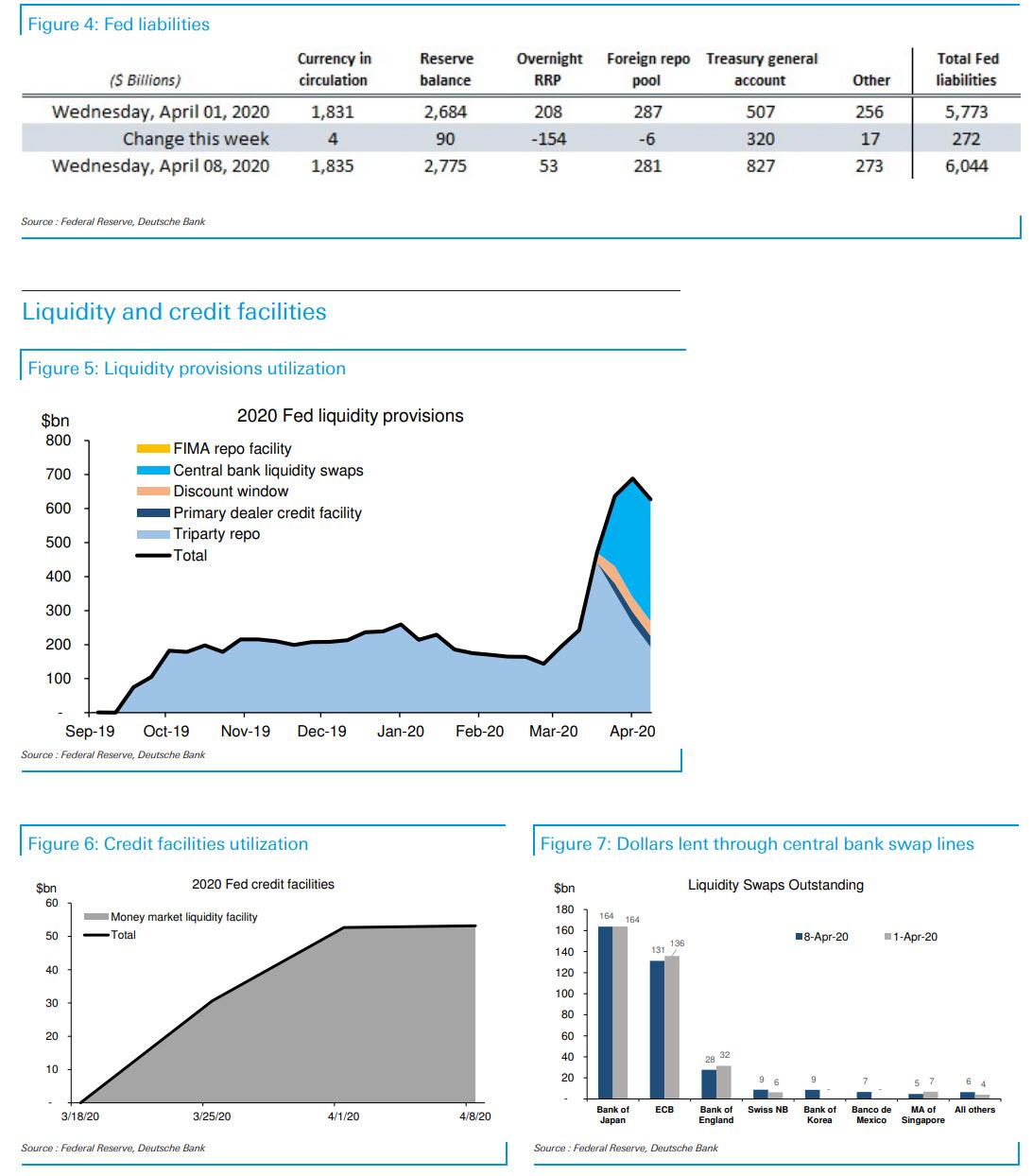

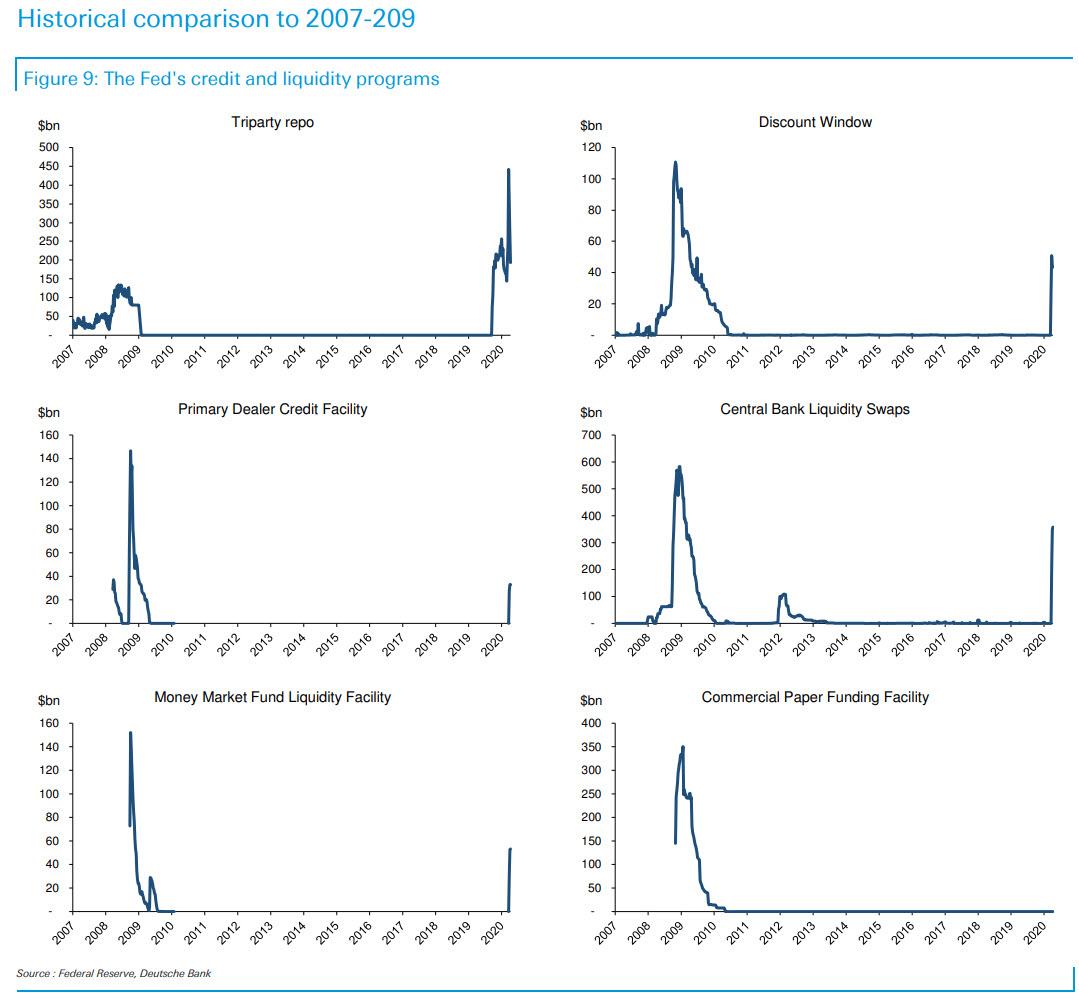

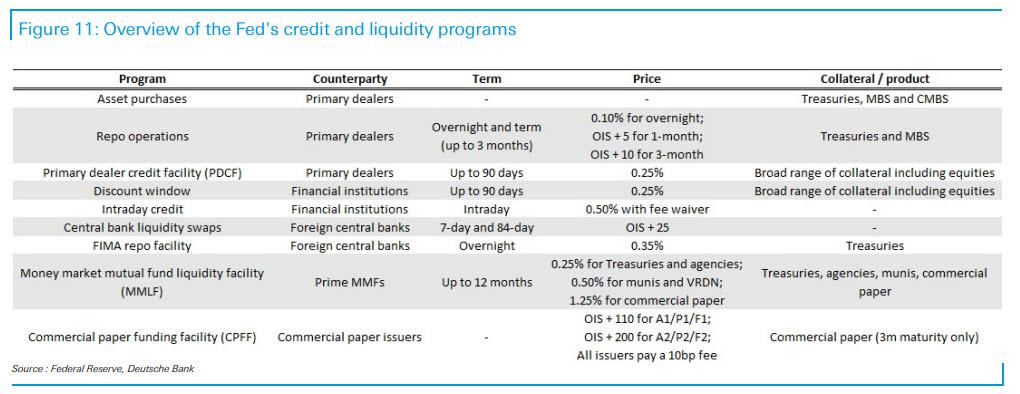

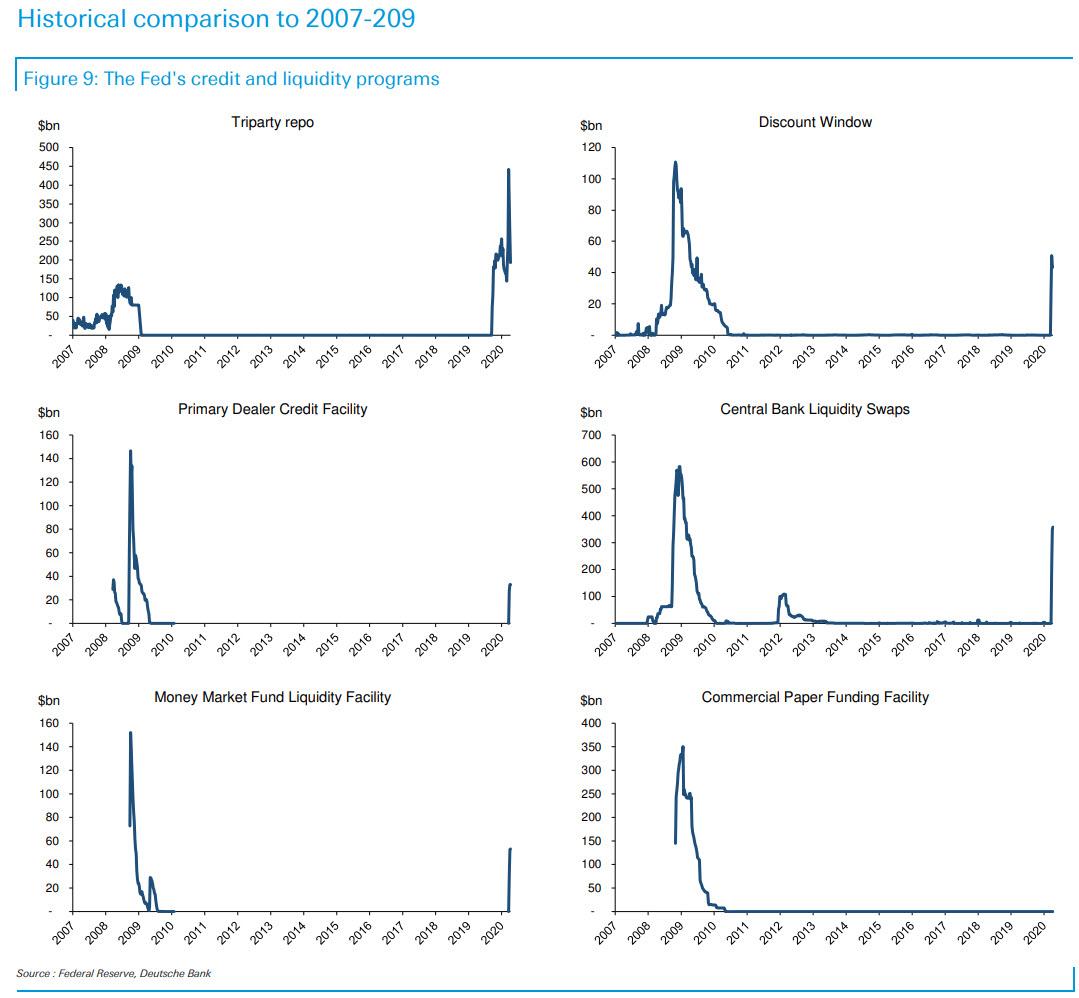

The highest utilization among the Fed’s credit facilities was

the central bank liquidity swap lines, which saw its balances increase

by $10bn to $358bn.

Temporary repo operations with primary dealers fell by $70bn to

$193bn. The newly introduced repo facility for foreign central banks had

a balance of only $1mm.

Balances in the Money Market Mutual Fund Liquidity Facility (MMLF)

and the Fed discount window were relatively unchanged from last week

with $53bn and $43bn, respectively.

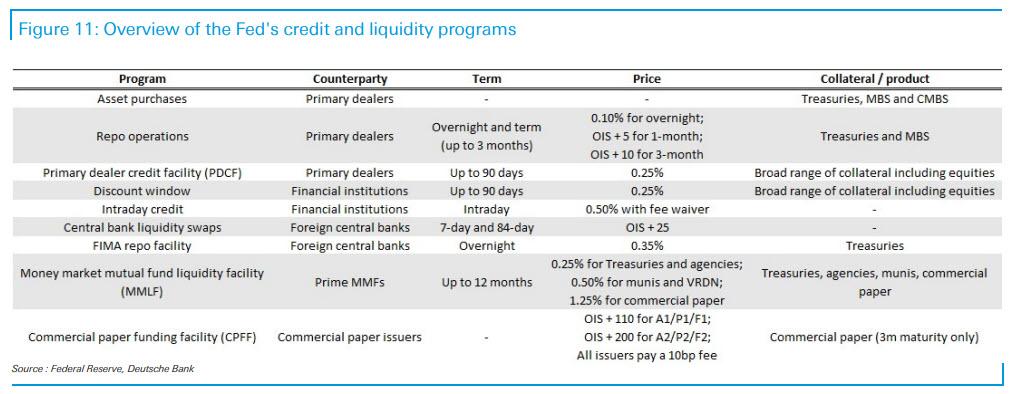

Then, to make sure the balance sheet goes even more exponential soon,

on Thursday, the Fed announced a new facility for municipal bonds and

details for a number of other programs, including the Main Street

Business Lending Program (MSBLP) and the corporate facilities. The two

corporate credit facilities will receive a combined $75bn, allowing for a

market footprint up to $750bn. Fed purchases will also include "fallen

angels" and portions of syndicated loans. In addition, a portion of its

ETF purchases in the Secondary Market Corporate Credit Facility will be

allocated to high-yield ETFs.

Meanwhile, the newly established Municipal Liquidity Facility will

offer up to $500bn of lending to states and municipalities backed by

$35bn in funding from the Treasury.

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....

Is The Stock Market As Confused As You Are About A Recession? Written by Lance Roberts | Apr, 1, 2019 Last week, Barron’s ran an article entitled “The Stock Market Is Just As Confused About A Potential Recession As You Are?” To wit: 先週バロンズにこういう記事が掲載された「株式市場は景気後退を予感させるほどに混乱しているだろうか?」見てみよう: “Investors have long used where we are in the economic cycle to decide which stocks to buy and sell. New research from Nomura’s Joseph Mezrich flips that on its head by showing how investors can use stock performance to help determine where we are in the cycle. Too bad the market is sending mixed messages right now.” 長らく投資家は現在景気サイクルのどこに居るかを見てこの株式を売るか買うかを判断してきた。野村證券のJoseph Mezrichの最近の研究では、これが逆さで、投資家は株式のパフォーマンスを見て今景気サイクルのどこにいるかを判断している。最悪なことに現在相場は悪化改善混在のメッセージを送っている。」 But let’s be clear here; no one wants the party to end. So, despite a struggling stock market over the last year, slowing economic growth, and a collapsing yield curve, there are s...