Back

in the days of the Fed's QE, much of thinking analyst world (the

non-thinking segment would merely accept everything that the Fed did

without question, after all their livelihood depended on it), was

focused on how massive, and shocking, the Fed's direct intervention in

capital markets had become. And while that was certainly true, what we

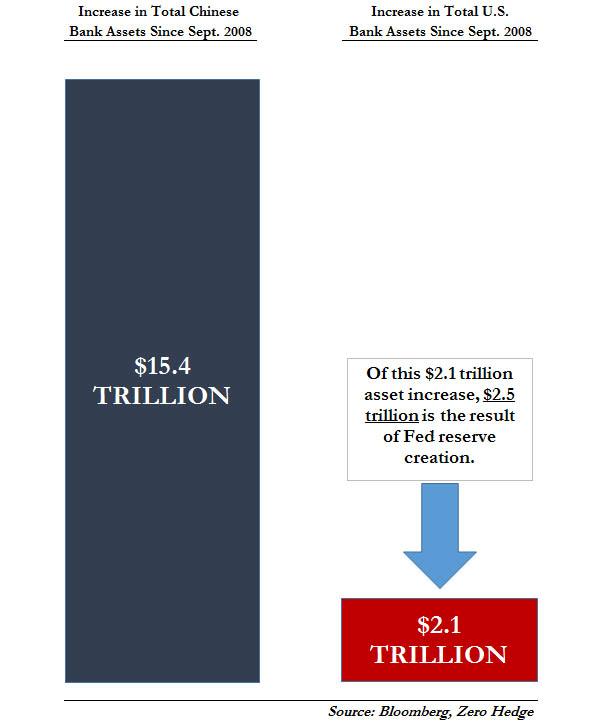

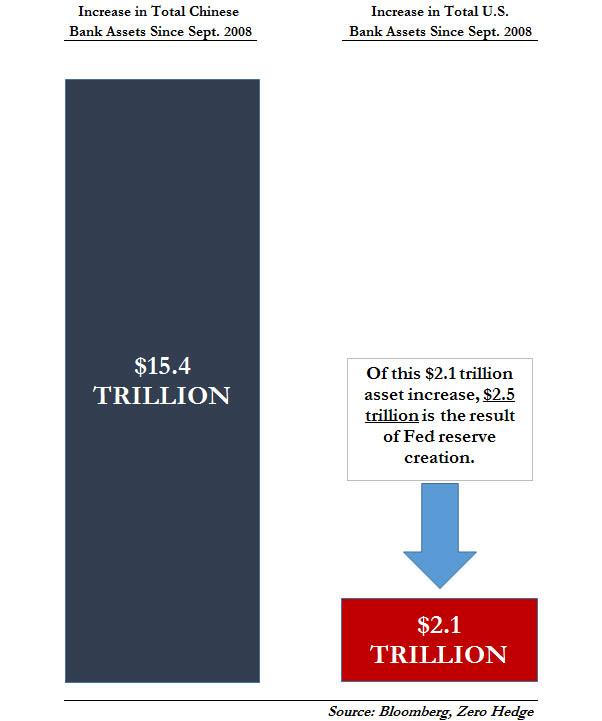

showed back in November 2013 in "Chart Of The Day: How China's Stunning $15 Trillion In New Liquidity Blew Bernanke's QE Out Of The Water"

is that whereas the Fed had injected some $2.5 trillion in liquidity in

the US banking system, China had blown the US central bank out of the

water, with no less than $15 trillion in increases to Chinese bank

assets, all at the behest of a juggernaut of new credit creation - be it

new yuan loans, shadow debt, corporate bonds, or any other form of debt

that makes up China's broad Total Social Financing aggregate.

FEDがQEを行っていた頃、思慮深いアナリストは(何も考えない人たちは疑問を持つことなくFEDのすることをすべて受け入れていた、結局彼らの生計はFEDに依存しているにすぎない)、それが如何に大きいか、またショッキングな出来事であるかに注目していた、FEDが直接資本市場に介入してきたわけなので。そしてそれはたしかに本当だったが、ZeroHedgeは2013年11月にこういう記事を示した「Chart of the Day: 中国はなんと$15Tの新規流動性を投入しBernankeのQEを打ちのめした」、FEDの流動性注入はわずか$2.5Tだったが、中国は米国中央銀行を打ちのめして、なんと$15Tもの流動性注入を行っった、圧倒的な新規与信生成によるものだったーー新たな人民元貸付、シャードー債務、企業債権、そのたあらゆる方法を駆使して中国の幅広い「社会融資総量 Total Social Financing」を積み上げた。

Now, almost six years later, others are starting to figure out what

we meant, and in an Op-Ed in the FT, Arthur Budaghyan, chief EM

strategist at BCA Research writes about this all important topic of

China's "helicopter" money - which far more than the Fed, ECB and BOJ -

has kept the world from sliding into a depression, and yet is blowing

the world's biggest asset bubble.

Budaghyan picks up where we left off, and notes that over the past decade, Chinese

banks have been on a credit and money creation binge, and have created

RMB144Tn ($21Tn) of new money since 2009, more than twice the amount of

money supply created in the US, the eurozone and Japan combined over the

same period. In total, China’s money supply stands at Rmb192tn, equivalent to $28 TRILLION.

Why does this matter? Because Chine money's supply is the size of broad

money supply in the US and the eurozone put together, yet China’s

nominal GDP is only two-thirds that of the US.

This, as the BCA analyst explains, is a major problem.

BCAアナリストの解説では、これが大きな問題だ。

Below we repost his latest FT Op-Ed, which explains why - as we said

in the 2019 year ahead post - we remain confident that the spark for

the next global financial crisis will be in China.

* * * China’s ‘helicopter money’ is blowing up a bubble, authored by Arthur Budaghyan is chief emerging market strategist at BCA Research, and first published in the FT. 中国の「ヘリコプターマネー」がバブルを膨らませている、著者 Arthur Budaghyan BCAリサーチ主任新興市場ストラテジスト、FTでの最初の記事。

The escalation of the trade conflict between the US and China has

raised the likelihood of greater stimulus by Beijing to prop up the

economy. While China’s excessive debt isn’t news, investors must wake up to the reality of “helicopter money” — enormous money creation by Chinese banks “out of thin air”.

While this sugar rush may provide short and medium-term cover for

investors, the long-term effects will exacerbate China’s credit bubble.

China, like any nation, faces constraints on frequent and large

stimulus, and its vast and still rapidly expanding money supply will

produce growing devaluation pressures on the renminbi.

When a bubble emerges we are often told that this bubble is

different. Many economists justify China’s credit and money bubble and

continuing stimulus by pointing to the nation’s high savings rate. But

this narrative is false. At its root is the idea that banks are

channelling or intermediating deposits into loans. This is not how banks

operate.

When a bank expands its balance sheet, it simultaneously creates an

asset (say, a loan) and a liability (a deposit, or money supply). No one

needs to save for this loan and money to be originated. The bank does not transfer someone else’s deposits to the borrower; it creates a new deposit when it lends.

In all economies, neither the amount of deposits nor the money supply

hinge on national or household savings. When households and companies

save, they do not alter the money supply.

Banks also create deposits/money out of thin air when they buy securities from non-banks. As banks in China buy more than 80 per cent of government bonds, fiscal stimulus also leads to substantial money creation. In short, when banks engage in too much credit origination — as they have done in China — they generate a money bubble.

Over the past 10 years, Chinese banks have been on a credit

and money creation binge. They have created Rmb144tn ($21tn) of new

money since 2009, more than twice the amount of money supply created in

the US, the eurozone and Japan combined over the same period. In total, China’s money supply stands at Rmb192tn, equivalent to $28tn. It

equals the size of broad money supply in the US and the eurozone put

together, yet China’s nominal GDP is only two-thirds that of the US.

In a market-based economy constraints are in place, such as the

scrutiny of bank shareholders and regulators, which prevent this sort of

excess. In a socialist system, such constraints do not exist.

Apparently, the Chinese banking system still operates in the latter.

There are clear downsides. Helicopter money discourages innovation

and breeds capital misallocation, which reduces productivity growth.

Slowing productivity and strong money growth ultimately lead to rising

inflation — the dynamics inherent to socialist systems.

Air show in Tianjin, China shows off China's helicopters. Getty Images.

In the long run, more stimulus in China will entail more money

creation and will heighten devaluation pressures on the renminbi. As we

all know, when the supply of something surges, its price typically

drops. In this case, the drop will take the form of currency

devaluation.

As it stands, China’s money bubble is like a sword of Damocles over the nation’s exchange rate.

Chinese households and businesses have become reluctant to hold this

ballooning amount of local currency. Continuous helicopter money will

increase their desire to diversify their renminbi deposits into foreign

currencies and assets. Yet, there is no sufficient supply of

foreign currency to accommodate this conversion. China’s current account

surplus has almost vanished.

As to the central bank’s foreign exchange reserves, at $3tn

they are less than a ninth of the amount of renminbi deposits and cash

in circulation. It is inconceivable that China can open its capital

account in the foreseeable future.

If China chooses the path of unrelenting stimulus, investors should

recognise the long-term negative outlook for the renminbi. Continuous

stimulus will beef up investment returns in local currency terms, but

currency depreciation will substantially erode returns in US dollars or

euros in the long run.

The investment implications go beyond Chinese markets. Market

volatility over the past few months as the talk of stimulus picked up

has given us a peek into the future. As the renminbi has

depreciated by 12 per cent since early 2018, the pain has reverberated

across Asian and other emerging markets. The MSCI Asia and MSCI

EM equities indices have each fallen 24 per cent in dollar terms since

their peak in January 2018. Long-term pressures could play out even more

dramatically.

Fortunately, Chinese authorities recognise these issues. Yet they

face an immense task of stabilising growth while containing credit and

money expansion. This will be hard to achieve in an economy that has

become addicted to credit creation.

多量のオピオイドを米国に送り込み、米国で深刻な麻薬中毒問題を引き起こしています。現代版「阿片戦争」です。あのトヨタ初の女性取締役もオピオイド中毒で逮捕解任されましたよね。 US Is Dependent On China For Almost 80% Of Its Medicine by Tyler Durden Fri, 05/31/2019 - 12:55 Experts are warning that the U.S. has become way too reliant on China for all our medicine , our pain killers, antibiotics, vitamins, aspirin and many cancer treatment medicine. 専門家はこう警告する、米国はすべての医薬品、痛み止め、抗生物質、ビタミン、アスピリン、各種抗がん剤で、中国依存度が高すぎる。 Fox Business reports that according to FDA estimates at least 80 percent of active ingredients found in all of America’s medicine come from abroad, primarily from China . And it’s not just the ingredients, China wants to become the world’s dominant generic drug maker. So far Chinese companies are making generic for everything from high blood pressure to chemotherapy drugs. 90 percent of America’s prescriptions a...

Amazonで買物をしてContrarianJを応援しよう Silver Outperforming Gold 2 Adam Hamilton July 26, 2019 3232 Words Silver has blasted higher in the last couple weeks, far outperforming gold. This is certainly noteworthy, as silver has stunk up the precious-metals joint for years. This deeply-out-of-favor metal may be embarking on a sea-change sentiment shift, finally returning to amplifying gold’s upside. Silver is not only radically undervalued relative to gold, but investors are aggressively buying. Silver’s upside potential is massive. ここ2週シルバーは急騰した、ゴールドを遥かに凌ぐものだ。これは注目すべきことだ、もう何年もシルバーはひどいものだった。この極端に嫌われた金属が大きく心理を買えている、とうとうゴールド上昇を増幅するに至った。シルバーは対ゴールドで極端に過小評価されているだけでなく、投資家は積極的に買い進んでいる。シルバーの潜在上昇力は巨大なものだ。 Silver’s performance in recent years has been brutally bad, repelling all but the most fanatical contrarians. Historically silver prices have been mostly ...

米国はよく理解してませんが、日本の場合では量的緩和で日銀が国債買い上げした資金は日銀当座預金にそのままです、市中には流れていません。でもNHKのニュース等では「ジャブジャブ」という表現をアナウンサーが使い、さらに丁寧に水道の蛇口からお金が吐き出される画像まで示してくれます。これって心理効果が大きいですよね。量的緩和とは何かを7時のニュースや新聞でこれ以上丁寧に解説するのはそう簡単ではありません。一般の人も株式をやっている人も「イメージ」で捉える以上はそう簡単にできません。多くの人は量的緩和とはなにか、を理解していないと私は想像しています。 ただし、国債を買い上げるので長期金利が低下し住宅ローン金利等が下がったのは確実な効果です。一方で長短金利差が少なくなると銀行のビジネスモデルが成り立たなくなりますが。 This Is The One Chart Every Trader Should Have "Taped To Their Screen" by Tyler Durden Sat, 01/19/2019 - 18:55 After a year of tapering, the Fed’s balance sheet finally captured the market’s attention during the last three months of 2018. 一年間のテーパリング後、FEDバランスシートがとうとう市場の注目をあびることになった、2018年の最後の3ヶ月だ。 By the start of the fourth quarter, the Fed had finished raising the caps on monthly roll-off of its balance sheet to the full $50bn per month (peaking at $30bn USTs, $20bn MBS...

結局、中国は隣国日本で20年前に起きたことを学んでいなかったということでしょう、というかどの国もどの政府も十分成熟するまでは「わかっちゃいるけどやめられない」ということでしょうね、きっと。 Spooked By Apple? Wait ‘Til China’s Bubble Bursts Written by Jesse Colombo | Jan, 3, 2019 Apple stock plunged nearly 10% on Thursday after the company cut its revenue forecast due to slowing iPhone sales in China. Apple’s woes dragged U.S. stock indices lower by more than 2% as fears of a more extensive China-driven slowdown spread. アップルの株価は火曜に約10%下落した、同社が中国でのiPhone売上原則を予想したためだ。アップルの弱さが米国株式指数を2%以上押し下げた、中国主導でさらなる原則が広がるのではという懸念からだ。 From the New York Times : ニューヨークタイムスによると: For years, no matter what was happening elsewhere, global companies bet billions upon billions of dollars that China’s consumers would keep spending money. 長年、他国で何が起きようとも多国籍企業は中国消費は巨額を維持することに賭けてきた。 Now, just when the world economy could use their financial firepower, they are no longer so quick to open their wallets. 今や、世界経済が金融弾薬を用いてももはや彼らの財布を緩めることはできない。 The latest sign of a slowdown in...

100年に一度と言われる出来事が過去20年で二回も起き、今度が三度目になるかどうか? Ignore The Yield Curve, They Said… 03-30-19 Written by Lance Roberts | Mar, 30, 2019 A Run For The Highs 高値に向かう Friday wrapped up the first quarter of 2019, and it was the best quarterly performance since 2009. As shown in the chart below, if you bought the bottom, you are “ killing it.” 2019Q1も金曜に終わり、2009年以来最良の四半期だった。下のチャートに示すが、もしみなさんが底値でかっていたなら、「息を呑まんばかりだ」ったろう。 However, you didn’t. しかしながら、そうはしなかったでしょう。 Despite all of the media “hoopla” about the rally, the reality is that for most, they are simply getting back to even over the last year. どのメディアもこのラリーで「大騒ぎ」だが、現実を思い起こすと、これは単に昨年のレベルに戻っただけのことだ。 That is, assuming you didn’t “sell the bottom” in December, which by looking at allocation changes, certainly appears to be the case for many. ということで、みなさんは12月の「底値で売る」ようなことをしなかったろう、それは多くの人も同じことだ。 If we deconstruct the ratio we can see the rotation a bit better この比率を分析すると資金移動をもう少しよく理解できる Not surpr...