流動性パニック:レポ危機始まり以来で最大のタームレポ需要となる、FEDは$94.5Bを注入し対処した

Update: 2月の月初にたしかに流動性が極端に枯渇した、先程FEDが一夜ものレポ市場に介入し、なんと$64.45Bを注入した・・・

... and which together with the massively oversubscribed $30BN term repo discussed below, means the Fed has injected $94.45BN in liquidity for today's market needs.

・・・それと同時に巨額の$30Bタームレポ需要があり、今日だけで市場の要求に応じて$94.45Bの流動性を注入した。

* * *

比較的平穏にリバースレポ市場は1月を終えたが、2月になって大暴れが始まった。

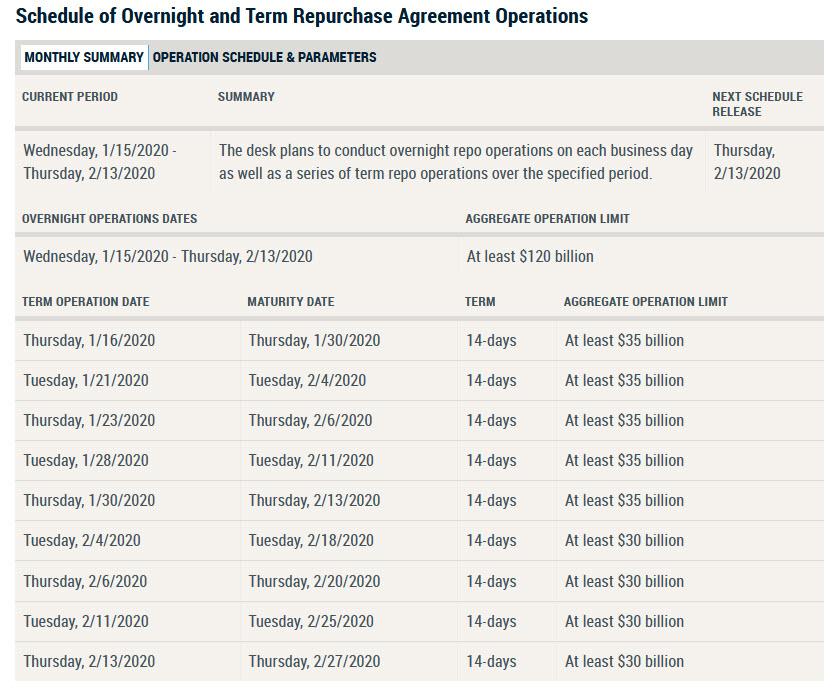

Even ahead of the results of today's reverse repo, some traders were already closely watching to see how it would play out for one main reason: as we reported on Jan 14, this was the first "tapered" reverse repo, whose aggregate operation limit was shrunk modestly from $35BN to $35BN.

今日のリバースレポ介入に先立ち、一部トレーダーはすでに注意深く見守っていた、その理由は:ZeroHedgeが1月14日に報告したように、今回が初めてのリバースレポの「テーパリング」だった、市場操作限度額が$35Bから$30Bに少し縮んだ。

There were also some questions why the repo would be tapered by only $5BN when the Fed repeatedly said the liquidity injection via repo were just a temporary operation (one which ostensibly should have ended soon after the September repocalypse), and yet which to this day continues to be an integral part of the Fed's balance sheet rebuild.

そこで多少の疑念が残っていた、どうしてテーパー額は$5Bに過ぎなかったのだろう、FEDは繰り返しレポ市場での流動性注入は一時的だと行っていたにも関わらずだ(建前上は9月のレポカリプス後にすぐに収束すべきだと行っていた)、それにも関わらず今日また引き続きFEDバランスシートを増やしている。

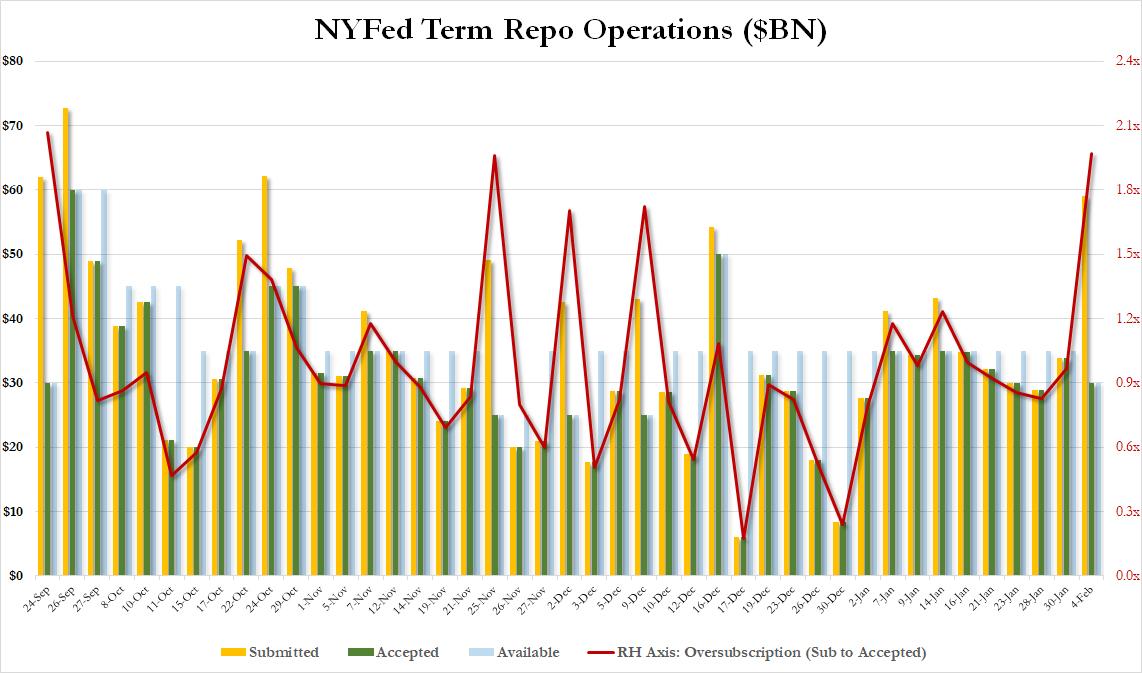

We got the answer moments ago, when the Fed announced that while the operation went off without a glitch, the demand for Fed liquidity was simply unprecedented, with $59.05BN in securities submitted ($41.75BN in TSYs, $17.3BN in MBS) for the downsized $30BN term repo maturing on Feb 18. As such, the nearly 2.0x submitted-to-accepted ratio made today's repo the most oversubscribed since the first term repo issued at the depth of the September repo crisis (and not by much), which saw $62BN in submissions for $30BN in liquidity.

ZeroHedgeはその答えを先ほど得た、市場操作を躊躇なく行うことをFEDが開示したが、FED流動性需要が単に前代未聞のものだったのだ、そこで$59.05Bの債権買取を行った、2月18日のタームレポ満期が$30Bと少ないにも関わらずだ。今日のレポ市場でsubmitted-to-accepted ratioが2.0xにもなり、昨年9月のレポ危機以来のものになった、$30Bの流動性に対して$62Bの申込みがあったのだ。

Ominously, the massive demand for term repo today means that the liquidity crisis that continues to percolate just below the surface of the market and has clogged up the critical plumbing within the US financial system, is getting worse, not better, and today's massive oversubscription indicates that one or more entities continues to face a dire shortage of reserves, i.e., cash. As for what they are doing with that cash, one look at Tesla this morning may provide an answer.

不吉なことに、今日のタームレポの巨額需要の意味するところは、水面下では流動性危機は継続しており、米国金融システムが詰まりそうになる臨界点に達している、これが今も悪化し続けている、改善していない、そして今日の巨額の需要の示唆することは、1社のみならず複数の機関が現金不足に直面しているということだ。その現金でやろうとしていることは、今朝のテスラの動向を見てもわかることだ。