市場のRepo依存症が悪化し、FEDは$83Bの流動性を注入

日本はGDPが500兆円程度で日銀の国債保有高も同程度です。これを参考にすると米国はGDPが2000兆円程度もあり、FEDのバランスシートはまだ400兆円程度なのでまだまだ余裕があります。大統領選挙まで毎月$100B(邦貨で10兆円)程度の流動性注入は余裕でできそうな気がします。少なくとも多くの市場参加者はそう思っているでしょう。

日本と同様に米国も量的緩和は一旦始まると、市場が督促するために、その限界まで「どうにも止まらない」ということになるようです。

だからといって株価がずっと上昇するかどうか、こればかりはわかりません。

FEDがレポ市場に資金を注入するため、これまでこの市場に投じられた資金が株式やもしかするとゴールド先物市場に押し出されているかもしれません。投機筋のロングポジションやオープンインタレストは過去最高になっています。

Fed Injects $83BN In Liquidity As Market's Repo Addiction Getting Worse

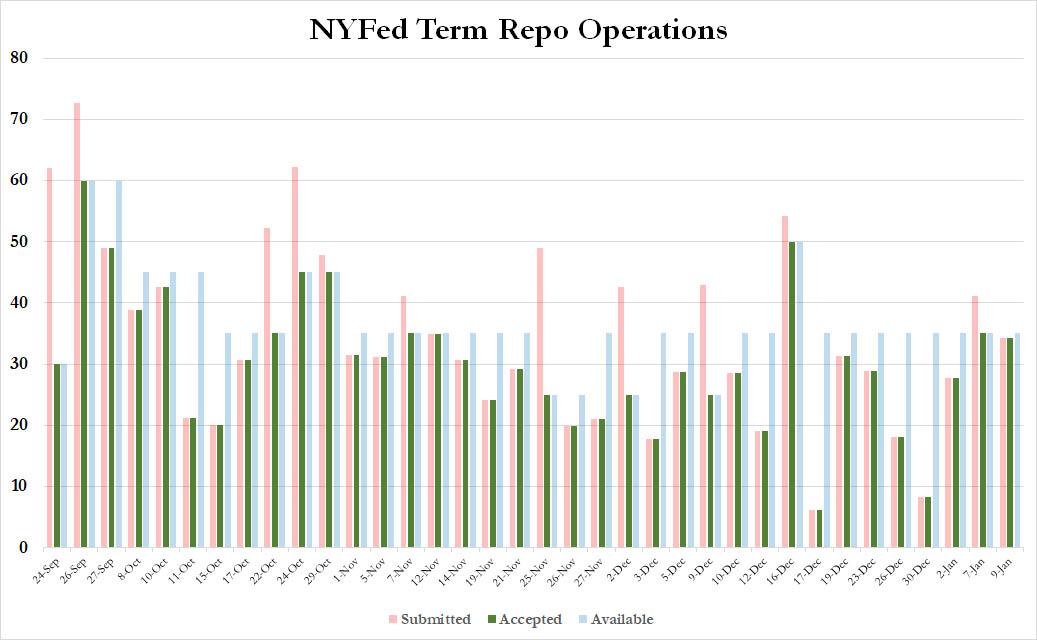

ZeroHedgeが記事を書いてから二日後に、またもや水面下でレポ市場に変調が置きているかもしれない、この三週間で初めて過剰申込みが置きた後、1月7日にFEDは期間2週で$35Bの予定のレポに対して$41.1Bの申込みを受けた、我々はFEDのレポ市場のイージーマネーに対して如何に多くの需要があるかを知ることになった、さきほどFEDは直近の2週term repo市場操作で過剰申込み状態に近かったことを開示した、$34.3Bの証券(短期証券$23.3B、MBS $11B)が今日の$35Bの市場操作に利用された、ディーラーは引き続きFEDへ流動性を提供するために緊急出動を継続している、もはは年末対策の「期間制限」ではないだけでなく、むしろ直接市場に資金を注ぎ込んでいる。

Today's operation, which was just shy of the maximum $35BN allowed, was the second highest term repo since Dec 16, and suggests that as repos are now maturing at a rapid burst (as we noted last week in "Mark Your Calendar: Next Week The Fed's Liquidity Drain Begins"), dealers remain as desperate as ever to roll this liquidity into newer term operations.

今日の公開市場操作では、設定された$35Bをほんの少し下回るだけであり、12月16日以来で二番目に大きなterm repo市場操作だった、今やterm reposの満期が爆発的に控えており(先週ZeroHedgeが記事にした「カレンダーに印をつけろ:来週からFEDの流動性引き去りが始まる」)、新たなterm repo 市場操作で、ディーラーはもう破れかぶれで繰延している。

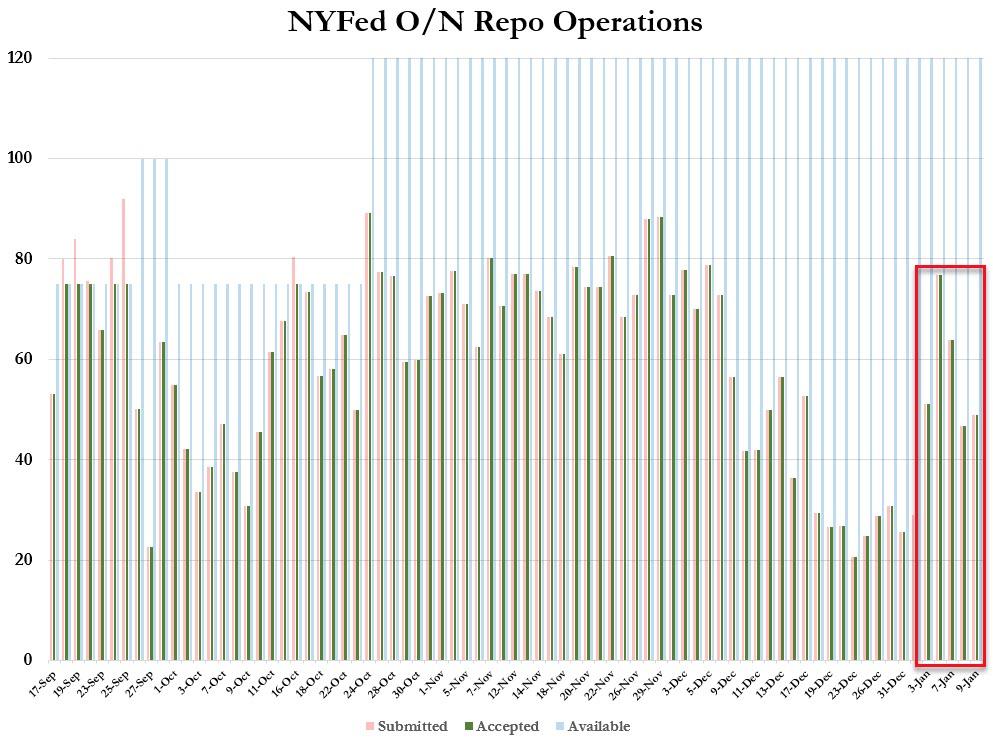

流動性不足が改善していないという疑いのもとで、その直後にFEDは連日の一夜ものrepo市場操作を開示した、$48.825Bの証券を買取(短期証券$24.2B、MBS $24.625B)というものだ、流動性注入は全体で$83Bを超えることになる!

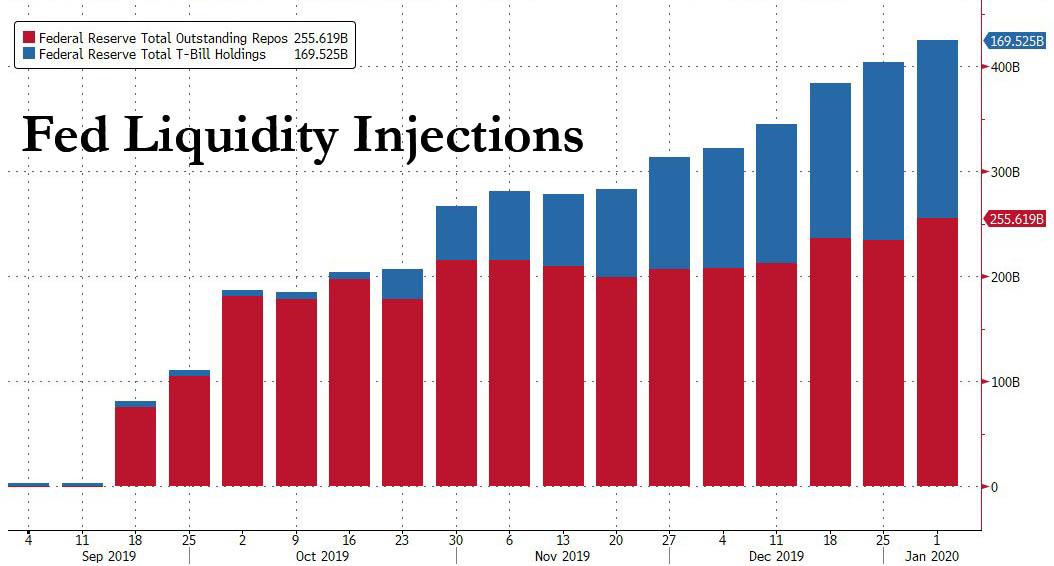

The latest repo operations also confirmed what we discussed overnight in "Top Repo Expert Warns Fed Is Now Trapped: "It Will Take Pain To Wean The Repo Market Off Easy Cash"" in which we noted that according to Curvature Securities' repo expert Scott Skyrm, something appears amiss as the total overnight and term Fed RP operations on Friday were greater than on year end! On year-end, the Fed had pumped a total of $255.95 billion into the market verses $258.9 billion on Friday.

直近のrepo市場操作に関してはZeroHedgeは昨夜議論した、この記事だ「Top Repo Expert Warns Fed Is Now Trapped: "It Will Take Pain To Wean The Repo Market Off Easy Cash」、このなかでZeroHedgeはCurvature Securitiesのレポ市場専門家Scott Skyrmの分析を引用した、そこで不都合が明らかになったが、金曜の一夜ものrepo,term repo FED市場操作総額は年末のものを超えるものだった!年末時点で、FEDは市場に$255.95Bを市場に注入していた、それが金曜には$258.9Bに増えていた。

The problem, as Skyrm explained, is that the market had gotten addicted to the easy Fed liquidity unleashed in September (via temporary repo ops), and then again in October (via permanent T-Bill purchases): "it's easy to see how the Repo market can get addicted to easy cash from the Fed when the stop-out rates for the RP operations are 1.55% - behind the offered side of the market." But, as the repo strategist added, as the Fed keeps injecting cash, the market gets used to it.

Which is great in the short-term as it sends risk assets soaring, but become a major issue over the long-term: "The long-term problem is that the some investor cash (real money cash) that was once going into the Repo market is now going elsewhere", Skyrm explains.

問題は、Skyrmが解説するように、9月にFEDが放出した流動性イージーマネーに市場が中毒になり(当時は一時的なrepo市場操作と言ってはいたが)、これが10月にも繰り返され(T-Bill短期証券買上げが恒常化し):「レポ公開市場操作の目標金利が1.55%で有ることを見ても分かる通りrepo市場はFEDのイージーキャッシュに中毒になっていることは明らかだ」。しかし、レポ市場の専門家はさらにこう言及する、FEDが現金を注入するだけ、市場はそれを利用する。これは短期的には素晴らしいことで、リスク資産を急騰させる、しかし長期的には大きな問題を伴っている:「長期的な問題は、かつてはレポ市場に投じられていた投資家の資金が今や他方面に投じられているということだ」、とSkyrm は解説する。

Indeed, the problem is that repo rates are trading in the lower end of the fed funds target range. When GC rates were higher in the range, Repo general collateral, as an investment, was more competitive than other overnight rates. But now that cash has gone to other markets.

たしかに、問題はレポ金利がFFRの目標金利下限になっていることだ。GCレポ金利がこのレンジよりも高ければ、他の一夜もの金利とレポ市場が投資対象として競合する。しかし今やその資金が他の市場に向かっている。

In short, just as the market got addicted to QE and the result was a

20% drop in the S&P in late 2018 when markets freaked out about

Quantitative Tightening, the Fed's shrinking balance sheet, and

declining liquidity, Skyrm cautions that "it will take pain to wean the Repo market off of cheap Fed cash" since "it's a circle" which can be described as follows:

要約すると、市場はQE中毒になっており、2018年遅くのように市場がQTでビビって流動性が欠如してしまうとS&P500が20%も下落することになる、Skyrmが警告するのは「FEDがチープマネーをレポ市場から引き去ると痛みが伴うだろう」というのも「これは資金流動の連鎖に組み込まれているからだ」これはこういうふうに解説される:

The problem is that stopping RP ops could spark another repo market crisis, especially with $259BN in liquidity pumped currently - more than at year end - via Repo. It also means that the Fed is now unilaterally blowing a market bubble with its repo and "NOT QE" injections, and yet the longer it does so the more impossible it becomes for the Fed to extricate itself from the liquidity pathway without causing a crash.

問題は、レポ市場操作をやめると再度レポ市場危機を引き起こすかもしれないことだ、特に現在は$259Bも流動性を注入しているーー昨年末よりも大きいーーこれがレポ市場に投入されている。この状況が意味することはFEDは今や一方的に市場バブルを吹き上げている、レポ市場操作と「NOT QE」注入によってだ、これが長引くほどに暴落なしにFEDは流動性引き去りをできなくなってしまう。

Or stated simply, the longer the Fed avoids pulling the repo liquidity band-aid, the bigger the market fall when (if) it finally does. The question then becomes whether Powell can keep pushing on the repo string until the November election, because a market crash in the months preceding it, especially since it will be of the Fed's own doing, will result in a very angry president.

もしくはもっと単純に言うと、FEDがレポ市場への流動性注入というその場しのぎを長引かせるほどに、最終的にその場しのぎができなくなるときの市場下落は大きくなる。問題はPowellがレポ市場操作を11月の選挙まで継続できるかだ、というのもFED自身の行動で選挙前数ヶ月に市場暴落を迎えると、大統領のとんでもない怒りを引き起こすだろう。

要約すると、市場はQE中毒になっており、2018年遅くのように市場がQTでビビって流動性が欠如してしまうとS&P500が20%も下落することになる、Skyrmが警告するのは「FEDがチープマネーをレポ市場から引き去ると痛みが伴うだろう」というのも「これは資金流動の連鎖に組み込まれているからだ」これはこういうふうに解説される:

For the Fed to end daily RP ops, they need outside cash to come back into the Repo market. For the Repo market to attract cash, Repo rates need to move higher. For rates to move higher, the Fed needs to stop RP ops.FEDが毎日のレポ市場操作をやめると、市場参加者は他の市場に投じていた資金をrepo市場に戻す必要がある。レポ市場が資金を引き寄せるためには、レポ金利が高くなる必要がある。金利が高くなると、FEDはレポ市場操作を止めざるを得ない。

The problem is that stopping RP ops could spark another repo market crisis, especially with $259BN in liquidity pumped currently - more than at year end - via Repo. It also means that the Fed is now unilaterally blowing a market bubble with its repo and "NOT QE" injections, and yet the longer it does so the more impossible it becomes for the Fed to extricate itself from the liquidity pathway without causing a crash.

問題は、レポ市場操作をやめると再度レポ市場危機を引き起こすかもしれないことだ、特に現在は$259Bも流動性を注入しているーー昨年末よりも大きいーーこれがレポ市場に投入されている。この状況が意味することはFEDは今や一方的に市場バブルを吹き上げている、レポ市場操作と「NOT QE」注入によってだ、これが長引くほどに暴落なしにFEDは流動性引き去りをできなくなってしまう。

Or stated simply, the longer the Fed avoids pulling the repo liquidity band-aid, the bigger the market fall when (if) it finally does. The question then becomes whether Powell can keep pushing on the repo string until the November election, because a market crash in the months preceding it, especially since it will be of the Fed's own doing, will result in a very angry president.

もしくはもっと単純に言うと、FEDがレポ市場への流動性注入というその場しのぎを長引かせるほどに、最終的にその場しのぎができなくなるときの市場下落は大きくなる。問題はPowellがレポ市場操作を11月の選挙まで継続できるかだ、というのもFED自身の行動で選挙前数ヶ月に市場暴落を迎えると、大統領のとんでもない怒りを引き起こすだろう。