Ever since the start of October when the Fed launched QE4 - or as

some still call it "Not QE" - in response to the Sept repo crisis,

figuring out the market has been pretty simple: if the Fed's balance

sheet goes up so does the S&P500, and vice versa.

The good news for traders is that for the past three months, the

Fed's balance sheet rose 11 of 12 weeks, and declined just 1 of 12, and

magically, the S&P did just that as well.

However, now that the year-end repo scare is history at least until

the April 15 tax date and certainly the next year end, it's time for the

Fed to start shrinking its balance sheet, mostly by allowing existing

term repo operations to expire without being rolled over. Conveniently,

the FOMC Minutes released moments ago provided the Fed's own big picture

take on when the massive liquidity injection since mid-September, which

expanded the Fed's balance sheet by $415BN in three and a half

months...

c

... with the Fed pointing out its "expectations to gradually

transition away from active repo operations [in 2020] as Treasury bill

purchases supply a larger base of reserves" and specifically, "the calendar of repo operations starting in mid-January could reflect a gradual reduction in active repo operations."

None of this is new, and it has almost become conventional wisdom

that when the Fed starts draining liquidity, the market impact will be

the polar opposite of what happened when it was injecting liquidity:

i.e., stocks will drop.

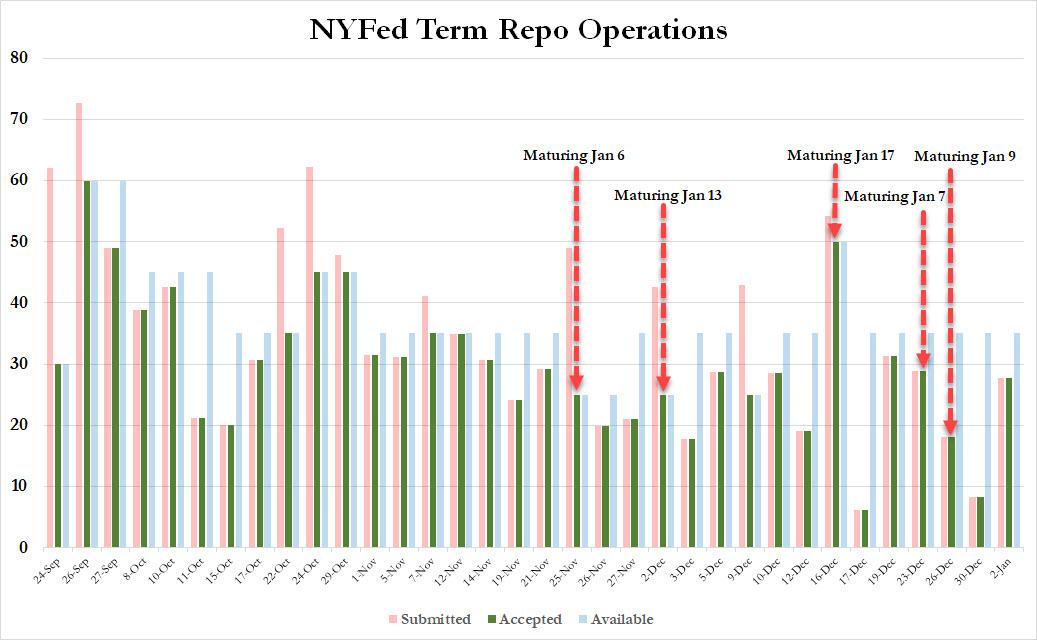

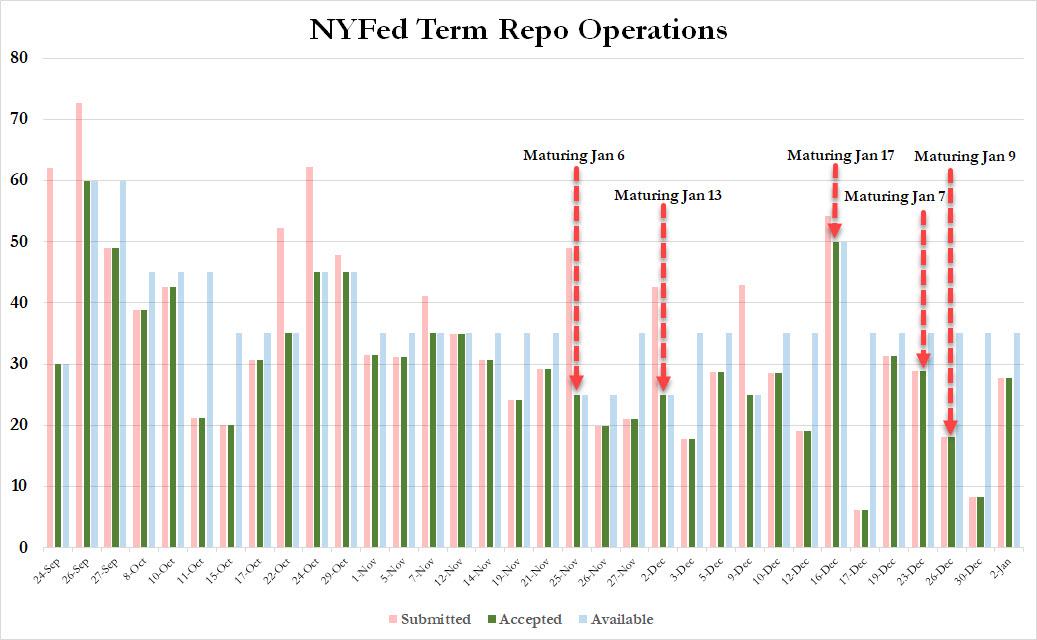

So with the Fed highlighting mid-January as the period when the

liquidity injection goes into reverse, here is some more details on just

which dates will be critical: as Curvature's Scott Skyrm points out,

these will be the days when the Fed's term repos maturing over the next

few weeks, supposedly without being rolled into further term repos, or

as he puts it, "during January, it will be interesting to see how the market reacts to the term RP ops maturing:" FEDは1月半ばに流動性注入が反転することを強調している、ここに示すのはそのなかでも重要な日付だ:Curvature社の Scott Skyrmが指摘するものだ、今後数週でFEDのterm reposが満期を迎えるだろう、term repoの繰延は無いと仮定している、彼の言によると「1月中に、term repo満期に市場がどう反応するか興味深いところだ:」

$25 billion leaves the market on Monday,

月曜には$25Bが市場から引き去られる、

$28.8 billion on Tuesday,

火曜には$28.8Bが引き去られる、

$18 billion next Friday, etc.

金曜には$18Bが引きさられる、というぐあいだ。

Of course, perhaps "interesting" is not the

right word, because it is clear that if liquidity is drained without a

matching injection, the market reaction will be anything but favorable.

That said, the Fed still has more term Repo ops scheduled to correspond

with those term roll-off dates, with at least three more term RP ops of

up to $35 billion scheduled in January. Whether or not banks decide to

use these to roll existing maturing term repos will determine if the

liquidity cliff starts hitting next week, or 3-4 weeks later. Finally,

it will also depend on whether the Fed decides that it had overinjected

the market with liquidity, and if it announces even more scheduled term

repos in February and onward.

当然のことだが、たぶん「興味深い」という言葉は適当ではない、というのも当分の注入なしに流動性が引き去られるのは明らかで、市場の反応は決して好感を持つものではないだろう。ということは、FEDは1月にまださらに term repoの満期を控えている。商業銀行が既存term repoの満期を繰延するかどうかで来週または3,4週後に流動性の崖が始まるかどうかが決まる。最終的には、FEDが市場に流動性を過剰注入するかどうかにかかっているだろう、そして2月以降のterm repoのさらなる対応スケジュール開示に依存する。

For now, however, here is a visual calendar of when some of the key December term repos mature over the next few days: