Authored by Mike Shedlock via MishTalk,

M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか?

Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US.

よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。

"There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. "

「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」

Clear Correlation? 明らかな相関?

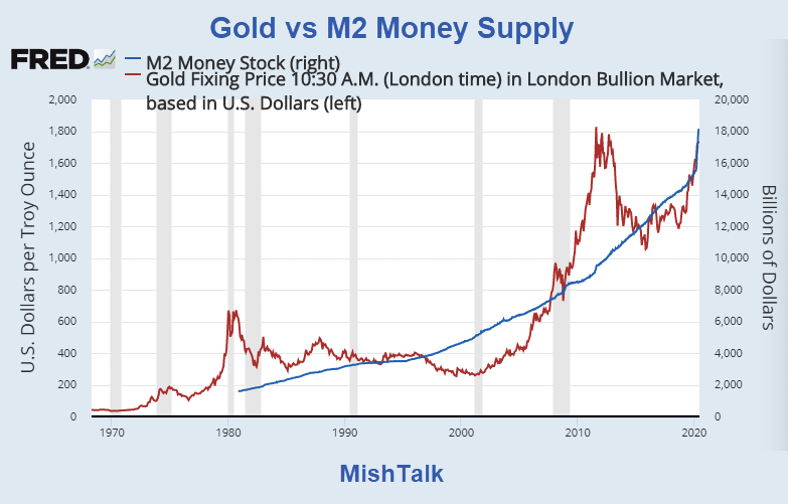

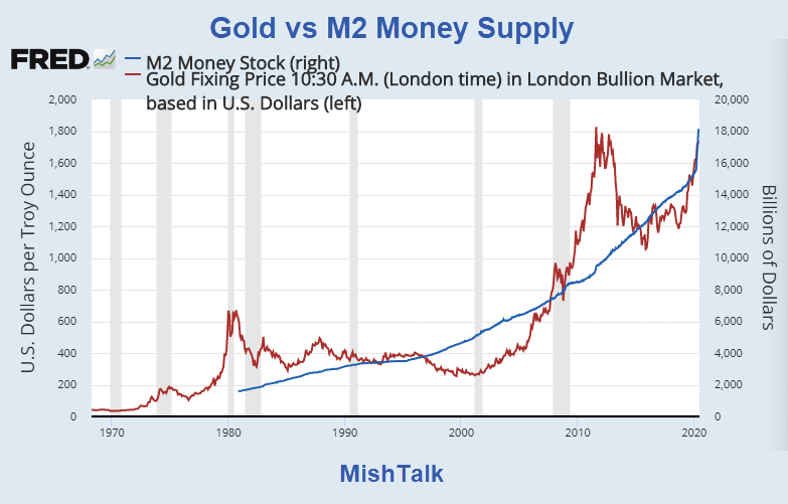

The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames.

If we look at longer time frames, the rate of increase in M2 theory falls flat on its face.

もっと長期間を見ると、M2増加率理論は意味を成さないことが解る。

One can force a correlation starting in 2010 but that is purposeful

cherry-picking a timeframe. and even then, the time period in the box is

counter-trend.

Similarly, one can find times when gold is correlated to the dollar,

the Yen, and most likely the popularity of peanuts at Cub games in some

time frame.

The best correlation I can find to the price of gold is faith in

central banks. Gold collapsed from $850 to $250 under Greenspan's "Great

Moderation". Greenspan was viewed as the "Maestro" until the dot-com

bubble collapsed.

Gold went on a tear during the housing bubble, but put in a top when ECB president Mario Draghi gave his famous speech: "We will do whatever it takes to save the Euro, and believe me it will be enough."

Draghi did nothing. His speech was enough. Bond yields on Greek,

Portuguese, and Italian bonds started collapsing right after that

speech. It was not until years later the ECB resorted to negative

interest rates and QE.

Gold started rising again when the ECB went nuts with QE and the Fed

started talking about "normalization"that anyone in their right mind

knew was not coming.

The BIS did a historical study and found routine price deflation was not any problem at all.

BISは長年物価デフレを研究してきた、そこに何ら問題はないという。

"Deflation may actually boost output. Lower prices increase real

incomes and wealth. And they may also make export goods more competitive,” stated the study.

It’s asset bubble deflation that is damaging. When asset bubbles burst, debt deflation results.

資産バブルデフレは損失を生み出す。資産バブルが破裂すると、債務デフレが生み出される。

Central banks’ seriously misguided attempts to defeat routine

consumer price deflation is what fuels the destructive build up of

unproductive debt and asset bubbles that eventually collapse.

Is The Stock Market As Confused As You Are About A Recession? Written by Lance Roberts | Apr, 1, 2019 Last week, Barron’s ran an article entitled “The Stock Market Is Just As Confused About A Potential Recession As You Are?” To wit: 先週バロンズにこういう記事が掲載された「株式市場は景気後退を予感させるほどに混乱しているだろうか?」見てみよう: “Investors have long used where we are in the economic cycle to decide which stocks to buy and sell. New research from Nomura’s Joseph Mezrich flips that on its head by showing how investors can use stock performance to help determine where we are in the cycle. Too bad the market is sending mixed messages right now.” 長らく投資家は現在景気サイクルのどこに居るかを見てこの株式を売るか買うかを判断してきた。野村證券のJoseph Mezrichの最近の研究では、これが逆さで、投資家は株式のパフォーマンスを見て今景気サイクルのどこにいるかを判断している。最悪なことに現在相場は悪化改善混在のメッセージを送っている。」 But let’s be clear here; no one wants the party to end. So, despite a struggling stock market over the last year, slowing economic growth, and a collapsing yield curve, there are s...