Authored by Alasdair Macleod via GoldMoney.com,

We are all used to the bullion banks covering their shorts on Comex

by waiting until the speculators are over-bullish and vulnerable to

mark-downs that trigger their stops. Algorithmic traders go from long to

short in a heartbeat as well, and they dump contracts into a falling

market, speeding up the decline. We should say at this juncture that the

Managed Money speculators are short-term, attracted by futures

leverage, and their gold position is often part of a wider risk strategy

deployed by hedge funds. They do not intend to stand for delivery. The

wider investment world taking strategic portfolio decisions does not

often get involved with gold, so the Comex gold contract has been a

secular play.

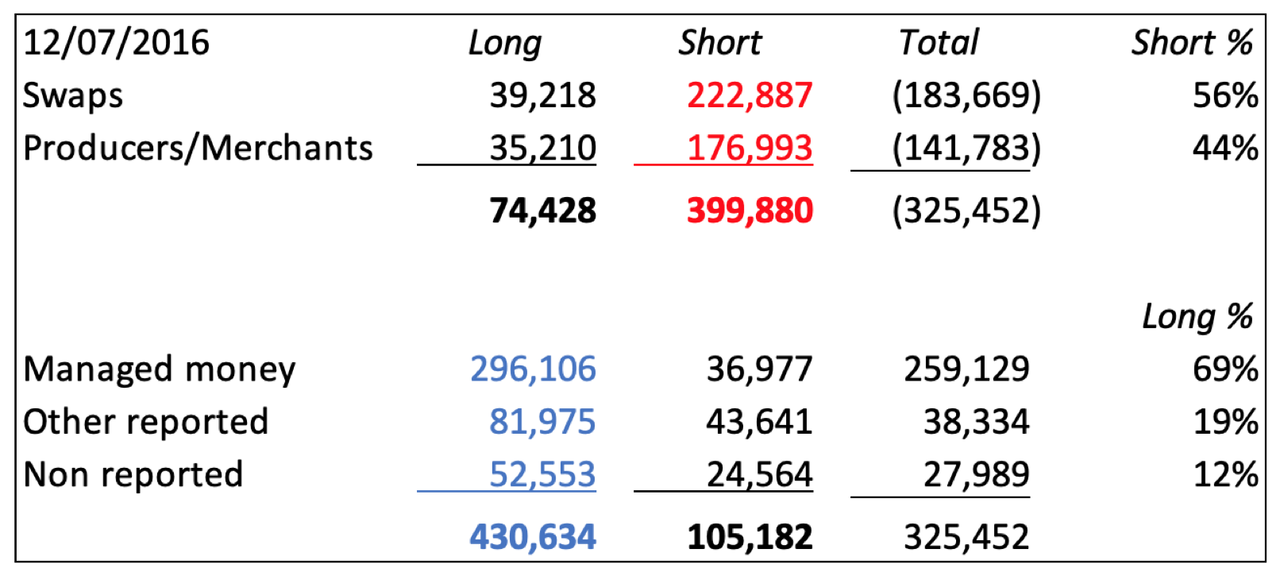

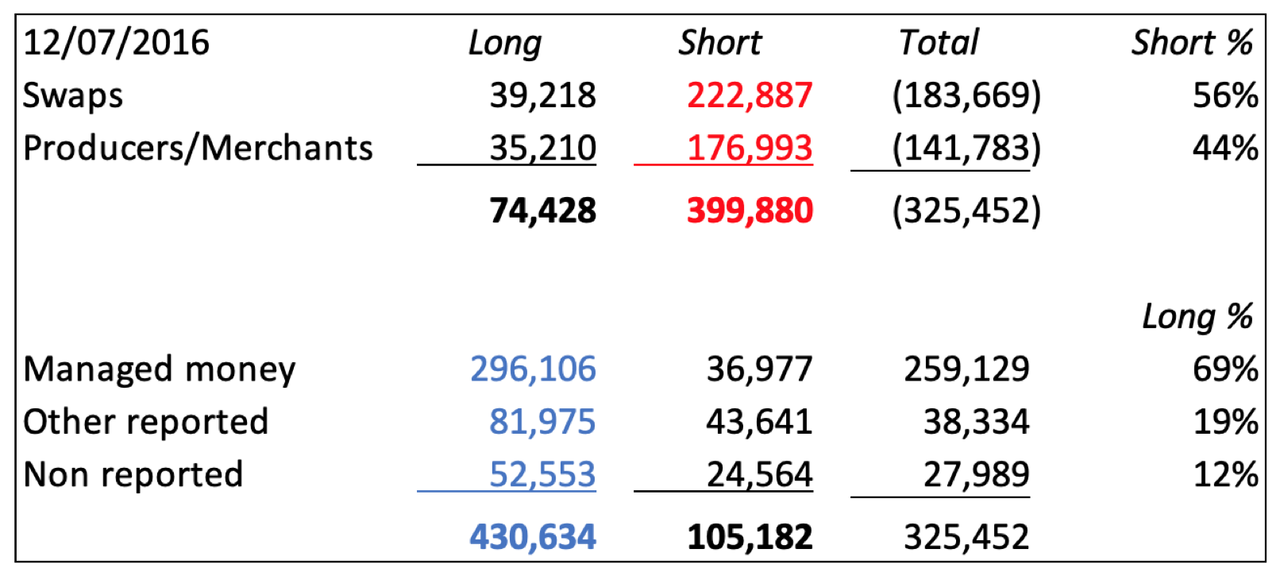

The table below shows a typical set-up, in this case July 2016. The

Managed Money category (296,106 — net 259,129 contracts) is close to

record long. Open interest was 633,000 contracts and the gold price was

at $1360, having run up from $1040 the previous December.

In the non-speculative category, the bullion banks (Swaps) had 56% of

the shorts and the Producer/Merchants 44%. Mark-to-market value of the

Swaps net short position was $25bn. Of the speculative longs, the

managed money category (hedge funds) held 69%, and at 296,106 long

contracts it was almost a record. There was a high level of bullishness;

easy pickings for the bullion banks, who by the following December

drove the price down to $1120, reducing their net shorts to under 50,000

contracts.

It was a game that evolved out of Comex futures being used simply to

offset long bullion positions at the LBMA. Over time, bullion bank

traders increased their trading position limits, as opposed to their

pure hedging activity, making easy money jobbing the other side of

Managed Money trades.

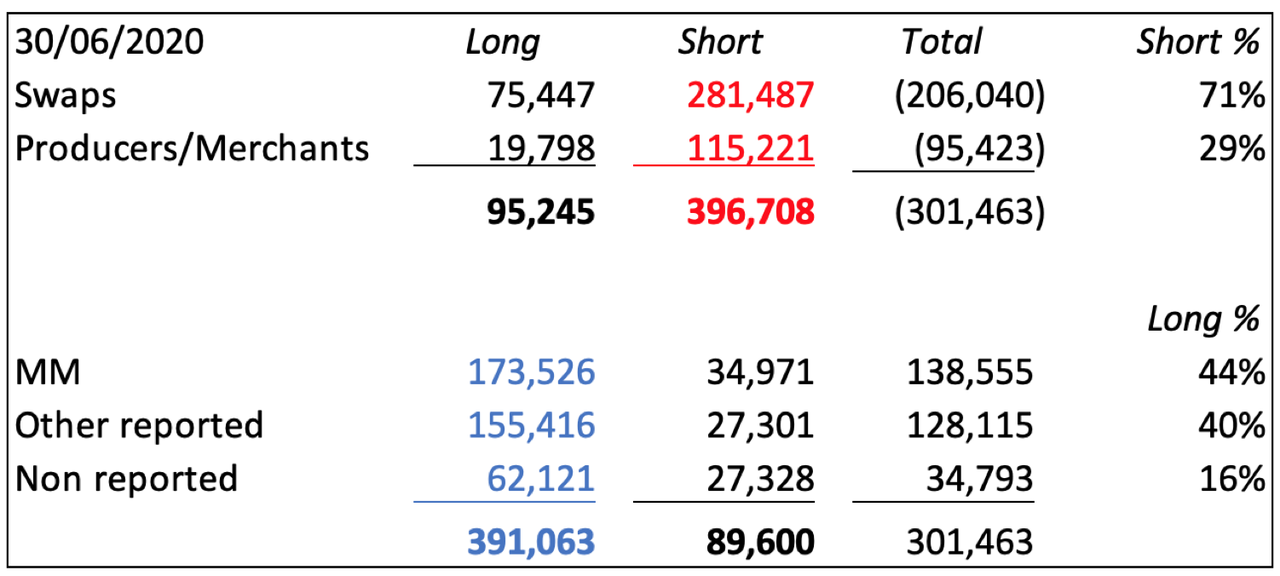

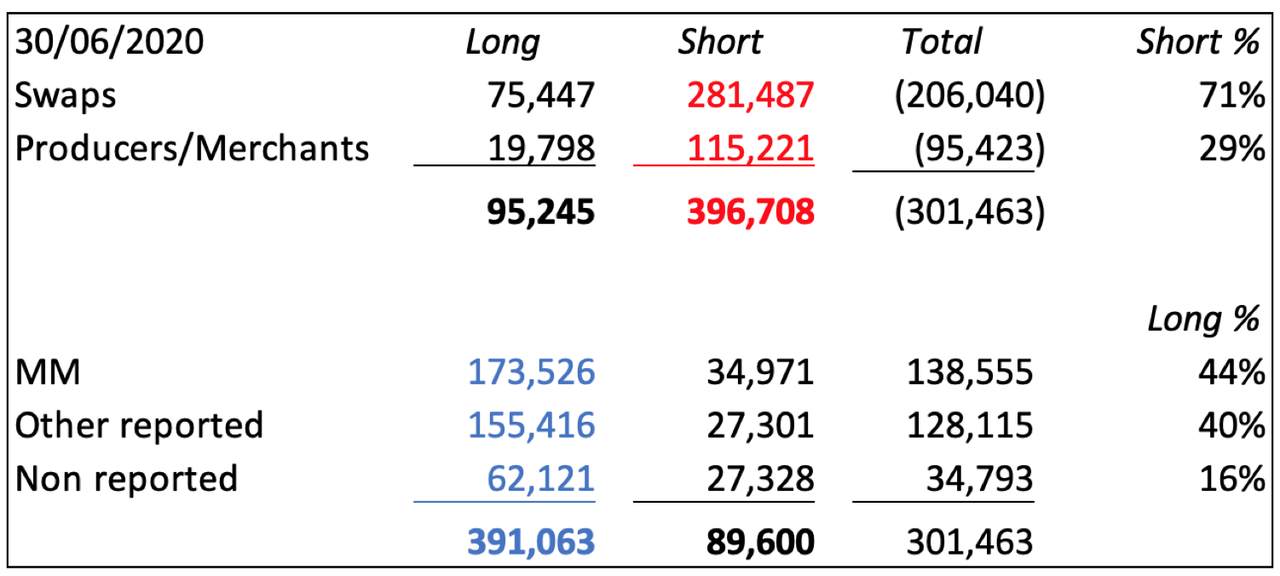

Now look at the current situation, with the gold price at decade highs ($1775) and open interest at 561,628 (30 June).

では、現在の状況を見てみよう、ゴールド価格は十年ぶりの高値($1775)になり、open interestは6月30日時点で561,628枚だ。

In the non-speculator category, the Swaps are more short than they

were in July 2016 despite open interest being 71,372 contracts lower.

The mark-to-market value is record net short at $36.6 billion. What has

happened is the Producer/Merchants have cut their positions, presumably

deciding that hedging mine output is less important in the current

inflationary environment. Consequently, the bullion banks are bearing

71% of the short exposure.

The speculator category makes this more interesting still. At 138,555

net long, hedge funds are only 25,000 contracts longer than average,

and compared with their bullishness in July 2016 have hardly got going.

It is the other categories, Other Reported and Non-reported have taken

56% of the long side, and they are not behaving like skittish hedge

funds at all. These include family offices, the ultra-wealthy and

foreigners through Globex who are standing for delivery as a means of

getting their hands on physical bullion —171 tonnes from the June

contract alone.

Bullion banks are between a rock and a hard place. For years they’ve

been playing the hedge funds as an angler hooks and plays a fish. That

game has ceased and there is no easy way for them to get level. For the

moment they are trying to put a lid on the price, but the cost has been

rising open interest, and therefore rising mark-to-market positions.

The August active contract runs off the board at the end of this

month and bullion banks are likely to be forced into large delivery

volumes again. Furthermore, the exchange for delivery arbitrage facility

between Comex and the LBMA is broken, allowing Comex premiums to London

spot to go unchallenged.

It is increasingly possible the gold contract is evolving into deep crisis, and that force majeure might have to be declared if, as seems increasingly inevitable, a wider banking crisis ensues.

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....